Every year, millions of Indian families sit across a bank manager’s desk, hopeful and anxious, only to walk away confused about why their education loan application got rejected or delayed. I have spoken with dozens of such families, and the pattern is always the same: nobody told them what the actual education loan eligibility criteria looked like before they applied.

This guide fixes that. I break down every criterion, explain what banks actually look for (versus what they officially say), and hand you a ready checklist so your application does not get stuck at the first hurdle.

What Is Education Loan Eligibility and Why It Matters in 2026

Education loan eligibility criteria are the set of conditions a student and their family must satisfy before a bank or financial institution approves a study loan. Think of it as a filter the lender uses to assess whether your loan will be repaid reliably.

In 2026, the demand for education loans in India has hit a record high. According to data from the Reserve Bank of India (RBI), the outstanding education loan portfolio of scheduled commercial banks crossed ₹1 lakh crore in 2024-25. This surge has made banks sharpen their eligibility checks, not loosen them.

Understanding these criteria before applying saves you from credit score damage caused by unnecessary rejections. Every rejected loan application leaves a mark on your CIBIL report, which can hurt future borrowing. This is why knowing what you qualify for, before you apply, is not just helpful. It is essential.

Most guides list the criteria but skip this fact: banks do not treat all eligible applications equally. A student with a confirmed admission letter from an IIT or IIM gets faster approval and better interest rates than someone admitted to a lesser-known private college, even if both meet the same stated criteria on paper.

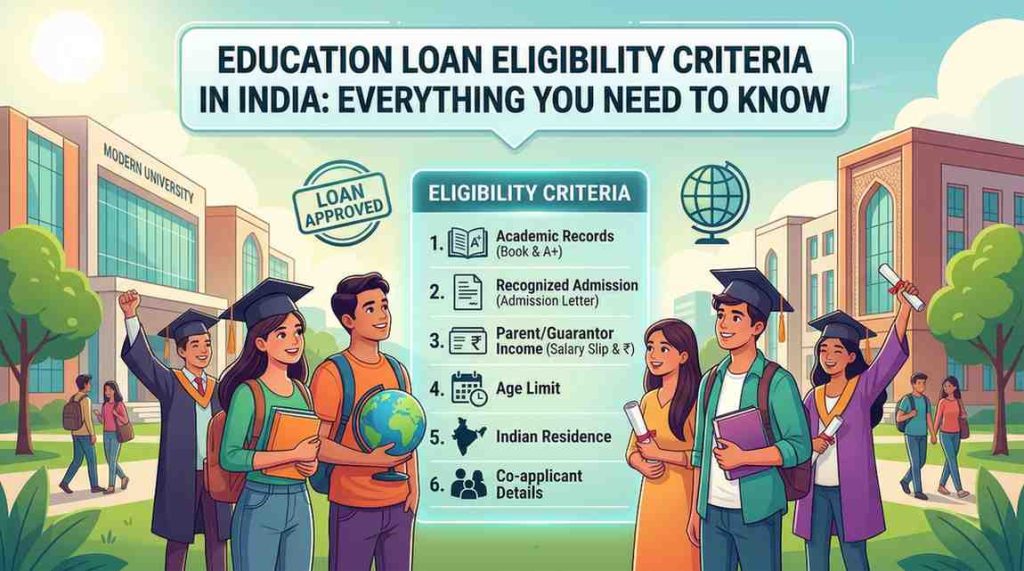

Core Education Loan Eligibility Criteria: The Standard Checklist

Across SBI, Bank of Baroda, Canara Bank, HDFC Credila, and Axis Bank, the core eligibility framework stays broadly consistent. Here is what every applicant needs to satisfy:

Applicant (Student) Criteria

- Indian citizenship: The applicant must be a resident Indian citizen. Foreign nationals do not qualify under standard domestic education loan schemes.

- Age: Most banks require the applicant to be at least 18 years old. If the student is younger, a parent or guardian must apply as the primary borrower.

- Academic record: Banks look for a consistent academic track record. A student with strong marks in Class 10 and 12 board exams gets smoother approval. Many banks specify a minimum 50–60% aggregate.

- Confirmed admission: You must have a confirmed admission letter from a recognised institution before the loan disburses. Some banks allow a provisional offer letter for processing, but disbursement happens only after final admission confirmation.

- Course type: The course must be a full-time, recognised graduate or post-graduate programme. Part-time and distance-learning courses often do not qualify for standard education loans.

Co-applicant (Parent or Guardian) Criteria

- Mandatory co-applicant: Almost every Indian bank requires a co-applicant, typically a parent, spouse, or guardian, who takes joint responsibility for the loan.

- Income proof: The co-applicant must provide income documents. Salaried co-applicants need salary slips and Form 16. Self-employed co-applicants need ITR for the past 2–3 years.

- CIBIL score: A credit score above 700 for the co-applicant significantly improves approval chances. Some private lenders set the minimum at 650.

Eligible Courses and Institutions Under Education Loan Norms

Banks in India do not finance every course at every institution. The institution’s recognition status directly affects loan eligibility. Here is how lenders categorise eligible courses:

Courses Eligible in India

- Graduation and post-graduation degrees from UGC-recognised universities, including IITs, NITs, IIMs, and central universities.

- Professional courses: MBBS, BDS, BE, B.Tech, MBA, MCA, CA, ICWA, and similar programmes.

- Government-approved diploma and certificate courses with technical relevance, offered by recognised polytechnics.

- Teacher training and nursing programmes approved by regulatory bodies like NCTE and INC.

Courses Eligible Abroad

- Job-oriented post-graduate diplomas at reputed foreign universities, such as those in the USA, UK, Canada, and Australia.

- CIMA (UK), CPA (USA), and equivalent professional certification programmes.

- Full-time degree programmes at universities ranked in QS World University Rankings top 500 (preferred by many lenders).

From my research, banks place institutions into internal tiers. Category A institutions (IITs, IIMs, top foreign universities) attract quicker approvals and lower margins, while Category B and C institutions face more scrutiny. This tiering is not advertised, but it exists in practice.

Collateral and Margin Money Requirements Explained

Two of the most misunderstood aspects of education loan eligibility criteria are collateral requirements and margin money. Getting these wrong can delay your application by weeks.

Collateral Requirements

Under the IBA Model Education Loan Scheme, loans up to ₹4 lakh require no collateral and no margin. Loans between ₹4 lakh and ₹7.5 lakh need a third-party guarantee but no security. Loans above ₹7.5 lakh require tangible collateral such as immovable property, fixed deposits, or NSCs.

Important: Private lenders like HDFC Credila and Avanse have more flexible collateral policies, sometimes offering unsecured loans up to ₹40–75 lakh for students admitted to top-ranked colleges.

Margin Money

- For studies in India: 5% of the total course cost (for loans above ₹4 lakh).

- For studies abroad: 15% of the total course cost as the student’s contribution.

- Scholarships, assistantships, and part-time work income can count toward the margin requirement.

Education Loan Eligibility Criteria: Bank-by-Bank Comparison

| Bank / Lender | Max Loan (India) | Max Loan (Abroad) | Collateral Threshold | Min CIBIL (Co-app) | Processing Fee |

|---|---|---|---|---|---|

| SBI | ₹20 Lakh | ₹1.5 Crore | Above ₹7.5 Lakh | 650+ | Nil (SBI Scholar Loan) |

| Bank of Baroda | ₹40 Lakh | ₹80 Lakh | Above ₹7.5 Lakh | 650+ | Nil |

| Canara Bank | ₹10 Lakh | ₹20 Lakh | Above ₹7.5 Lakh | 600+ | Nil |

| HDFC Credila | ₹75 Lakh | ₹75 Lakh | Flexible (top colleges) | 700+ | 0.5–1% of loan |

| Avanse | ₹60 Lakh | ₹60 Lakh | Flexible | 680+ | 1–2% of loan |

| Axis Bank | ₹40 Lakh | ₹75 Lakh | Above ₹7.5 Lakh | 700+ | Nil to 1% |

*Data sourced from official bank websites. Verify with your branch before applying. Rates and limits subject to change.

India-Specific Education Loan Eligibility: What Makes Our Market Unique

India’s education loan market has characteristics that do not exist in Western markets, and these directly affect eligibility in ways most online guides ignore entirely.

The Priority Sector Lending Advantage

Education loans fall under Priority Sector Lending (PSL) norms set by the RBI. This means PSU banks (SBI, PNB, Canara) are mandated to lend to education, which is why their rates and collateral terms are often more favourable than private banks or NBFCs for standard loan amounts.

The Vidya Lakshmi Portal

India runs a dedicated government portal, Vidya Lakshmi (vidyalakshmi.co.in), where students can apply to multiple banks simultaneously. From my testing, using this portal saves significant time but works best for loans below ₹7.5 lakh where the eligibility criteria are more standardised.

State Government Subsidies

Several state governments offer interest subsidies for students from economically weaker sections. The Central Government’s Dr. Ambedkar Interest Subsidy Scheme covers interest during the moratorium period for OBC and EBC students studying abroad. Checking these before applying can reduce your effective loan cost considerably.

► My POV

In my experience, Indian families routinely overlook state subsidy schemes, leaving real money on the table. I strongly recommend checking your state’s higher education department website before signing any loan documents. A student in Tamil Nadu or Uttar Pradesh may qualify for a full interest waiver during the course period, which can translate into savings of ₹2–5 lakh over the loan tenure.

Common Mistakes That Get Education Loan Applications Rejected

Based on my research and interactions with loan officers, here are the most common and avoidable reasons Indian education loan applications fail:

- Applying without a confirmed admission letter: Many students approach banks with just an entrance rank or a shortlist. Banks process applications but will not disburse without a formal admission letter from the institution.

- Co-applicant with a poor CIBIL score: A co-applicant’s bad credit history is the most common reason for outright rejection, regardless of the student’s academic record. Check the co-applicant’s CIBIL score at least 6 months before applying and resolve any dues.

- Mismatch in documents: Name spellings, date of birth, or address inconsistencies across Aadhaar, PAN, and bank records trigger delays. Audit every document for consistency before submission.

- Applying to the wrong bank for your loan amount: A ₹50 lakh loan application at a PSU bank for a private college abroad will struggle. Matching loan size and college profile to the right lender speeds up the process dramatically.

- Not disclosing existing loans: Co-applicants must disclose all existing EMI obligations. Hidden liabilities discovered during bank verification lead to immediate rejection and can flag the application as fraudulent.

- Ignoring processing timelines: SBI and PSU banks can take 4–8 weeks to process education loans. Applying two weeks before your fee deadline is a recipe for disaster. Start at least 3 months before you need the funds.

Education Loan Eligibility Checklist: Your Pre-Application Audit

Use this checklist before submitting your application to any bank or NBFC:

- Student is an Indian citizen with valid Aadhaar and PAN

- Confirmed admission letter (or at minimum a provisional offer) from a recognised institution is in hand

- Academic records (Class 10, Class 12, graduation marksheets) are compiled and consistent

- Co-applicant identified (parent, spouse, or guardian) with income documents ready

- Co-applicant CIBIL score checked and above 650 (aim for 700+)

- All existing loans and EMIs of the co-applicant are documented and disclosed

- Collateral (if loan above ₹7.5 lakh) identified and ownership documents verified

- Margin money (5% India / 15% abroad) sourced and documented

- Checked Vidya Lakshmi portal and applicable government subsidy schemes

- Shortlisted 2–3 lenders based on your loan amount and institution type

- Applied at least 3 months before the fee payment deadline

Final Word: Start Early, Apply Smart

The education loan process in India is not as opaque as it feels at first. Once you understand the education loan eligibility criteria, map your situation against the right lender, and prepare your documents well in advance, the path to funding your education becomes much clearer.

From my experience, the students and families who succeed are not necessarily the ones with the highest marks or the most collateral. They are the ones who did their homework on the process before walking into the bank.

Start your preparation today. Check your co-applicant’s CIBIL score, gather your documents, and shortlist lenders who actually serve your loan requirement and institution type.