Money should never be the reason a bright student stays home while others go ahead.

That is exactly the problem the Vidya Lakshmi Portal was built to solve. I have seen too many students from small towns and middle-class families in India give up on their dream college simply because they did not know how to get a loan, or who to ask. This portal changes all of that in a single window.

In this guide, I walk you through everything you need to know about the Vidya Lakshmi Portal education loan, from registration and eligibility to filling the form, tracking your status, and understanding the new PM Vidyalakshmi Scheme benefits in 2026.

Key Takeaways

- The Vidya Lakshmi Portal lets you apply to up to three banks with one form (CELAF).

- The PM Vidyalakshmi Scheme (launched November 2024) adds collateral-free loans, credit guarantee, and interest subvention for QHEI students.

- Students with family income up to ₹8 lakh get 3% interest subvention on loans up to ₹10 lakh during the study and moratorium period.

- 860+ institutions qualify as QHEIs, including IITs, NITs, IIMs, and state government colleges ranked between 101–200 in NIRF.

- 75% credit guarantee by the government covers loans up to ₹7.5 lakh, making banks more willing to lend.

- Loan repayment can stretch up to 15 years, making EMIs manageable on a starting salary.

- The entire process is digital — no bank branch visit needed to apply.

Quick Facts: Vidya Lakshmi Portal at a Glance

| Detail | Information |

|---|---|

| Official Portal URL | pmvidyalaxmi.co.in / vidyalakshmi.co.in |

| Launched By | Ministry of Finance + Ministry of Education + IBA |

| Operated By | Protean eGov Technologies (formerly NSDL e-Gov) |

| Banks on Portal | 45+ registered banks |

| Loan Schemes Available | 139 education loan schemes |

| Max. Collateral-Free Loan | Up to ₹7.5 lakh (credit guarantee by Govt.) |

| Interest Subvention | 3% for family income up to ₹8 lakh (on loans up to ₹10 lakh) |

| Applications Per Student | Up to 3 banks at once via one CELAF form |

| Repayment Tenure | Up to 15 years |

| Moratorium Period | Course duration + 1 year |

| PM Vidyalakshmi Launch | November 6, 2024 (Cabinet approved) |

| Scheme Budget (2024–2031) | ₹3,600 crore |

| Eligible Institutions (QHEIs) | 860+ top-ranked institutions (NIRF-based) |

Read More: Section 80E Tax Benefit on Education Loan: Complete Guide (FY 2025-26)

What Is the Vidya Lakshmi Portal?

The Vidya Lakshmi Portal is the Government of India’s official single-window platform where students can search, compare, and apply for education loans from multiple banks. using just one form.

Before this portal existed, a student had to visit 4 or 5 different bank branches, fill out different forms, and wait separately at each one. The process was exhausting, confusing, and often unfair to students who did not have contacts inside banks.

The portal solves this completely. You register once, fill out the Common Education Loan Application Form (CELAF), and submit it to up to three banks at the same time. Every participating bank receives your application, evaluates it, and responds to you directly through the portal.

The portal is developed and managed jointly by the Ministry of Finance, the Ministry of Education, and the Indian Banks’ Association (IBA), and is operated by Protean eGov Technologies. It also links directly to the National Scholarship Portal, so you can check scholarship options alongside your loan application.

What Is the PM Vidyalakshmi Scheme? (2024 Update You Must Know)

Many students confuse the old Vidya Lakshmi Portal with the newer PM Vidyalakshmi Scheme. Here is how to understand the difference clearly.

The Vidya Lakshmi Portal has existed since 2015. In November 2024, the Union Cabinet approved a new Central Sector Scheme called PM-Vidyalaxmi, which upgraded the portal’s benefits significantly. The PM Vidyalakshmi Scheme now sits on top of the existing portal, offering better terms specifically for students admitted to top-ranked institutions.

Here is what the PM Vidyalakshmi Scheme adds:

- Collateral-free and guarantor-free loans for students admitted to Quality Higher Education Institutions (QHEIs) — no property pledge, no co-signer required for most cases.

- 75% credit guarantee by the Government of India for loans up to ₹7.5 lakh, which means banks lend more freely because the government backs them.

- 3% interest subvention on loans up to ₹10 lakh for students from families with annual income up to ₹8 lakh. This subsidy applies during the moratorium period (course period + one year).

- For families earning up to ₹4.5 lakh, full interest subvention is already available under the earlier PM-USP CSIS scheme for technical/professional courses.

- The scheme targets around 22 lakh students across 860 QHEIs, with 7 lakh fresh students expected to benefit from interest subvention annually.

What are QHEIs? Quality Higher Educational Institutions are colleges and universities ranked in the top 100 in NIRF overall, category-specific, or domain-specific rankings. State government institutions ranked between 101 and 200 in NIRF also qualify.

Who Is Eligible to Apply on the Vidya Lakshmi Portal?

Eligibility requirements split into two layers: the basic loan eligibility and the additional requirements for PM Vidyalakshmi benefits.

Basic Eligibility for Education Loan on the Portal

- Must be an Indian citizen

- Must have completed Class 10+2 (or equivalent)

- Must have a confirmed admission letter from a recognized institution

- Age typically between 18 to 35 years (varies by bank)

- A co-applicant (usually a parent or guardian) is required for most loans

- Co-borrower is mandatory for all loans above ₹75 lakh under PM Vidyalakshmi variants

Additional Eligibility for PM Vidyalakshmi Benefits

- Must have secured admission through competitive exam or merit-based selection at a QHEI

- The institution must appear on the official QHEI list published at dashboard.aishe.gov.in

- Family income must be up to ₹8 lakh per year (for 3% interest subvention)

- Must not be receiving any other Central or State government scholarship or interest subvention

- Must not have been dismissed for academic or disciplinary reasons

Documents Required to Apply

Getting your documents ready before you sit down to fill the form saves a lot of time. From my experience, incomplete document uploads are the number one reason applications get delayed at the bank level.

Identity and Address Proof:

- Aadhaar Card (mandatory for KYC)

- PAN Card

- Passport (if applicable, especially for abroad studies)

Academic Documents:

- Class 10 marksheet (your name as registered here matters)

- Class 12 marksheet

- Graduation marksheets (if applying for postgraduate loan)

- Entrance exam result / merit list

- Admission letter from the institution

- Fee structure / demand letter from the institution

Income Documents (for interest subvention):

- Income certificate for the family

- Bank statements (6 months) of co-applicant

For PM Vidyalakshmi Interest Subvention Specifically:

- Declaration that no other Central/State scholarship or subsidy is being received

Keep originals ready, the bank may ask to verify them physically after the portal submission.

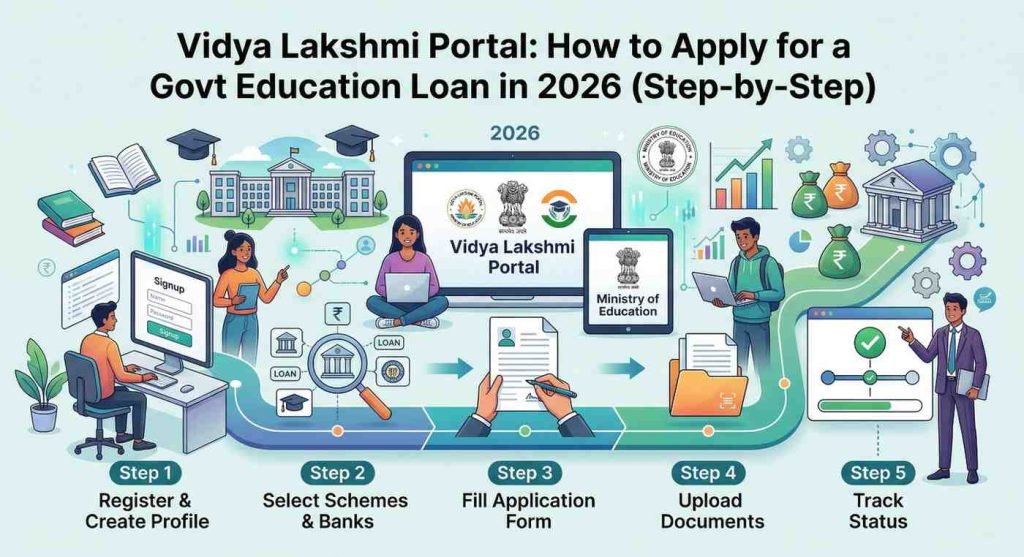

How to Register on the Vidya Lakshmi Portal (Step-by-Step)

Step 1: Go to the Official Portal

Visit pmvidyalaxmi.co.in or vidyalakshmi.co.in, both take you to the same platform. Do not use third-party websites claiming to register on your behalf. Always use the official government URL.

Step 2: Click on “Student Login / Register”

On the homepage, find the “Student Login” button. Below it, you will see a “Register Here” link for first-time users. Click that.

Step 3: Fill the Registration Form

Enter your details:

- Full name exactly as it appears on your Class 10 marksheet

- Mobile number (used for OTP)

- Email ID (this becomes your login ID permanently)

- Password of your choice

- CAPTCHA code

After submitting, check your email for an activation link. Click it to activate your account. If the activation email does not arrive within 10 minutes, check your spam folder.

Step 4: Log In to Your Dashboard

Return to the portal and click “Student Login.” Enter your email ID, password, and the CAPTCHA. Click Submit. Your student dashboard will open.

Step 5: Search for Loan Schemes

Click on “Search for Loan Scheme” in the menu. Enter:

- Location of study (India or abroad)

- Course type (undergraduate, postgraduate, diploma, etc.)

- Loan amount required

The portal shows you a list of matching banks and their loan schemes with interest rates, limits, and terms. Compare at least three banks before choosing.

Step 6: Fill the CELAF Form

Click “Apply” against your chosen bank scheme. This opens the Common Education Loan Application Form (CELAF). The form has seven sections:

- Instructions

- Basic information

- Personal information

- Present banker details

- Course details

- Cost and financial information

- Document upload

Fill each section carefully and click “Save and Next” after each one. On the final page, review everything, then click Submit.

Step 7: Apply to Up to 3 Banks

You can submit the same filled CELAF to up to three banks. Each bank receives it independently and processes it separately. This increases your chances of approval.

► MY POV: I strongly recommend applying to all three bank slots rather than waiting for one bank to respond first. Banks take 15 to 30 working days on average. If one bank delays or rejects, you lose time waiting. Applying to three at once protects you and keeps your options open.

How to Check Vidya Lakshmi Portal Loan Application Status

After you submit, tracking your status is simple.

- Log in to your portal account

- Click on “Application Status” or go to “My Applications”

- Use your Application ID or Student ID to pull up the current status

- The system shows you which bank has received it, whether it is under review, and any documents or queries pending from the bank

If a bank does not respond within 30 days: Log back in, raise a grievance through the portal’s grievance section, or contact the bank’s nodal officer directly. The government guidelines do not allow indefinite silence on applications.

Comparison: Old Vidya Lakshmi Portal vs. PM Vidyalakshmi Scheme (2026)

| Feature | Old Vidya Lakshmi Portal | PM Vidyalakshmi Scheme (2024 Onward) |

|---|---|---|

| Collateral Requirement | Required for loans above ₹7.5 lakh | Collateral-free for QHEIs regardless of amount |

| Credit Guarantee | Limited | 75% Govt. guarantee for loans up to ₹7.5 lakh |

| Interest Subvention | Only under CSIS for income under ₹4.5 lakh | 3% for income under ₹8 lakh on loans up to ₹10 lakh |

| No. of Banks | 45+ | Same banks, expanded schemes |

| Eligible Institutions | All recognized institutions | Focus on 860+ QHEIs (NIRF-ranked) |

| Application Method | Digital via CELAF | Same CELAF, now on pmvidyalaxmi.co.in |

| Scholarship Link | National Scholarship Portal | National Scholarship Portal (continued) |

| Interest Payment | Standard EMI | Via e-voucher and CBDC wallet |

India-Specific Angle: Why This Portal Matters for Indian Students in 2026

India produces millions of college-going students every year. Yet according to data from the Department of Higher Education, a significant number of students from families in the ₹4–8 lakh annual income bracket fall into a gap, they earn too much to qualify for many full-fee waivers, but not enough to self-finance a top college education.

The PM Vidyalakshmi Scheme directly addresses this group. With a total budget of ₹3,600 crore sanctioned for 2024-25 through 2030-31, it aims to benefit roughly 22 lakh students across India’s top-ranked institutions.

For students in states like Uttar Pradesh, Bihar, Rajasthan, and Madhya Pradesh, where bank branch access is still limited in semi-urban areas, the entirely digital nature of this portal is a big deal. You do not need to travel to a city branch. You register from your phone or a cyber cafe, upload your documents, and track everything online.

One angle most articles miss: the portal also works for students applying to central government institutions like IITs, NITs, IIMs, and AIIMS. These are automatically on the QHEI list, which means their students automatically qualify for PM Vidyalakshmi benefits. If you are an IIT student or NIT student reading this, you likely qualify, and you may not even know it.

Common Mistakes Students Make on the Vidya Lakshmi Portal

From what I have seen and researched, these are the errors that most often delay or reject applications:

Wrong name in the registration form. The portal asks for your name as per your Class 10 marksheet. Many students enter a nickname or a casual spelling. The bank then flags a name mismatch when it verifies documents. Always match exactly.

Applying before getting the admission letter. The CELAF form requires your institution and course details confirmed by an admission letter. Some students apply speculatively before getting confirmation. Banks reject these applications immediately.

Not checking if the college is on the QHEI list. If you want PM Vidyalakshmi benefits, your institution must appear on the approved QHEI list. Check at dashboard.aishe.gov.in before you apply. Applying through the portal without confirming this wastes your time and the bank’s.

Uploading blurry or cropped documents. The portal has specific file size and clarity requirements. A blurry Aadhaar scan or a cropped income certificate causes banks to put your application on hold for re-upload, which costs you days.

Waiting for one bank before applying to others. You can apply to three banks at once. Many students apply to just one bank and wait weeks. If that bank delays or rejects, they start from scratch. Use all three slots.

Ignoring the moratorium period. Repayment does not start immediately. Most banks give you the full course duration plus one year before the first EMI kicks in. Many students panic thinking they must repay immediately. You do not.

Conclusion: Take the First Step Today

The Vidya Lakshmi Portal removes almost every excuse for not pursuing higher education due to financial reasons. One form, one registration, and access to 45+ banks, all from your phone or laptop.

If you have a confirmed admission letter and your documents are ready, you can complete the registration and submit your Vidya Lakshmi Portal education loan application in under an hour.

The PM Vidyalakshmi Scheme makes 2026 an especially good year to apply, the interest subvention, collateral-free guarantee, and digital processing are all active. Do not wait for someone to hand this information to you. The portal is live at pmvidyalaxmi.co.in. Go register today.

For the official list of eligible institutions, visit: https://dashboard.aishe.gov.in

GradsLoan: The Smartest Way to Fund Your Higher Education

If you want a faster, simpler alternative to navigating multiple bank portals, GradsLoan is worth a serious look. In my experience, GradsLoan cuts through the paperwork and connects students directly with the right lender for their profile, no branch visits, no confusion.

Whether you need a loan for an IIT, NIT, or a top private college, GradsLoan helps you compare options and get approval without the usual back-and-forth.

Do not let funding delays cost you your seat. Contact GradsLoan today and take the first step toward your dream education.

Disclaimer: This article is for informational purposes only. Loan terms, interest rates, and eligibility conditions are set by individual banks and the Government of India and may change. Always verify current details on the official Vidya Lakshmi Portal before applying.

Frequently Asked Questions

What is the official website of the Vidya Lakshmi Portal?

The official URLs are pmvidyalaxmi.co.in and vidyalakshmi.co.in. Both lead to the same platform. Always use these government links and avoid third-party websites that claim to help with registration.

How many banks are registered on the Vidya Lakshmi Portal?

As of 2026, more than 45 banks are registered on the portal, offering 139 education loan schemes. Major banks include SBI, Bank of Baroda, Canara Bank, Punjab National Bank, Union Bank of India, and HDFC Bank.

Can I apply for an education loan if my family income is above ₹8 lakh?

Yes. The income limit applies only to the 3% interest subvention benefit. The education loan itself is available to students of all income groups through the portal, and the collateral-free guarantee also applies regardless of family income for loans up to ₹7.5 lakh.

How long does it take for a bank to approve a Vidya Lakshmi loan application?

On average, the approval process takes 15 to 30 working days from the date of application. The timeline depends on your document completeness, the bank’s internal processing, and any queries the bank may raise. Applying to three banks at once reduces wait risk.

Can I edit my application after submitting it on the portal?

You can edit the application only before final submission. Once submitted, log in, go to “My Applications,” and click “Edit” next to the relevant application. After final submission, you cannot edit, but you can withdraw and reapply.

What happens if I do not get admission to a QHEI? Can I still use the portal?

Yes. The Vidya Lakshmi Portal works for students at all recognized institutions, not just QHEIs. The PM Vidyalakshmi-specific benefits (collateral-free loan guarantee, 3% subvention) apply only to QHEI students. But you can still apply for regular education loans from all 45+ banks through the same CELAF form.

Is the Vidya Lakshmi Portal safe? Will my data be secure?

Yes. The portal is managed by Protean eGov Technologies under the oversight of the Ministry of Finance and Ministry of Education. It uses standard government-grade security protocols. Never share your portal password with anyone, including people who claim to be bank representatives.

What is the repayment tenure for a Vidya Lakshmi education loan?

Repayment tenure typically goes up to 15 years, depending on the loan amount and the bank’s specific scheme. Repayment begins after the moratorium period (course period + one year), giving you time to find a job before your first EMI.