Most students celebrate the moment their education loan gets approved. But here is what I have noticed in years of tracking the student finance space in India: the confusion starts right after that celebration. What exactly is this document you just received? Can you show it to a university? Will the embassy accept it? What comes next?

The education loan sanction letter is the single most important document in your entire loan journey, and most guides explain it so poorly that students end up making costly mistakes during the visa stage.

In this guide, I cover everything, what the sanction letter means, every component inside it, the difference between a pre-approved and a final letter, how long it stays valid, whether it is enough for your visa, and exactly what you must do after receiving it.

Key Takeaways

- The education loan sanction letter is a formal commitment from your lender, not a fund transfer. Money moves only after the loan agreement is signed.

- The letter contains your loan amount, interest rate, tenure, moratorium period, EMI, and disbursement conditions. Read every line before proceeding.

- Two types exist: in-principle letters (conditional, pre-admission) and final sanction letters (unconditional, post-documentation). Use the final letter for visa applications wherever possible.

- Validity is typically 3 to 6 months. Set a reminder before it expires.

- For study-abroad visas, the sanction letter is essential financial evidence but may need to be accompanied by bank statements showing liquid funds for UK visa applications specifically.

- Post-sanction steps, loan agreement, disbursement schedule, collateral registration, are as important as getting the sanction itself.

Quick Facts: Education Loan Sanction Letter at a Glance

| Detail | Information |

|---|---|

| What it is | Official document confirming loan approval |

| Issued by | Bank, NBFC, or government lending institution |

| When issued | After credit assessment, before loan agreement |

| Validity period | Typically 3 to 6 months (varies by lender) |

| Accepted for | University admission confirmation, visa application |

| Does it mean money is released? | No — disbursement happens after the loan agreement |

| Key contents | Loan amount, interest rate, tenure, moratorium, EMI |

| Two types | In-principle/Pre-approved letter vs Final sanction letter |

| India’s key lenders | SBI, HDFC Credila, Axis Bank, Avanse, Auxilo, Tata Capital |

What Is an Education Loan Sanction Letter?

An education loan sanction letter is an official written confirmation from a bank or NBFC stating that your loan application has been assessed and approved. It communicates the lender’s decision and lays out the exact terms under which the loan will be disbursed.

Think of it as the bridge between application and actual money. The bank has reviewed your documents, evaluated your creditworthiness and your co-applicant’s income, and decided to lend you a specific amount. The sanction letter formalises that decision in writing.

This is not the same as receiving the funds. The sanction letter is a commitment, not a transfer. The actual release of money, called disbursement, happens only after you sign a formal loan agreement and submit additional documents like your university admission letter and fee demand notice.

What makes this document uniquely important in India is its dual-use function. Universities abroad need proof that you can fund your education before confirming your seat. Embassies processing student visas, for countries like the USA, UK, Canada, and Australia, require evidence of financial backing. The sanction letter serves both purposes, making it a document you will use far before the first rupee actually moves.

Components of an Education Loan Sanction Letter

Understanding what the sanction letter contains is not a formality. Each line in this document directly affects your repayment burden for the next 10 to 15 years of your life.

Loan Amount

This is the total amount the lender agrees to fund. It may cover tuition fees, living expenses, travel costs, and study materials depending on what you applied for and what the bank assessed as reasonable. Always verify that the sanctioned amount actually covers your full cost of attendance, including living costs if you are studying abroad, not just tuition.

Interest Rate

The letter specifies whether the rate is fixed or floating. Most Indian banks offer floating rates linked to their MCLR (Marginal Cost of Funds Based Lending Rate) or Repo Rate. A 0.5% difference in rate on a loan of Rs. 40 lakh over 10 years can change your total repayment by Rs. 2 to 3 lakh. Read this line carefully and compare it against what other lenders offered you.

Loan Tenure

This is the total repayment period, typically 10 to 15 years for education loans in India. The tenure begins after your moratorium period ends.

Moratorium Period

This is the repayment holiday. Most lenders offer a moratorium that covers your course duration plus 6 to 12 months after course completion or first employment (whichever is earlier). During the moratorium, you do not pay EMIs, though interest typically continues to accrue.

EMI Amount

The letter mentions the EMI that will apply after the moratorium ends. This calculation is based on the principal amount plus accrued interest.

Collateral or Security Conditions

If your loan is secured, the letter specifies what collateral you have pledged, its assessed value, and any conditions related to it.

Conditions Precedent

This section lists what the bank requires from you before it releases the first disbursement. Typical conditions include a university admission letter, visa stamp, fee demand notice from the institution, and completion of the loan agreement.

Types of Education Loan Sanction Letter

Not every sanction letter carries the same weight or finality. Understanding the difference between the two types prevents serious mistakes during the university admission and visa stages.

In-Principle or Pre-Approved Sanction Letter

This is a conditional approval issued before you have a confirmed university admission. Some lenders issue this to help students demonstrate financial capability during the application stage.

An in-principle letter states that the bank is willing to lend up to a certain amount, subject to conditions such as receiving a confirmed offer letter from the university and completing the full documentation process.

Several universities in the USA, Canada, and Australia accept this letter for issuing an I-20, CAS letter, or offer of admission. However, not all embassies treat it as equivalent to a final sanction letter for visa purposes. Always check the specific requirements of the embassy where you are applying.

Final Sanction Letter

This is the complete, unconditional approval issued after your full documentation, including your university admission letter, has been verified. The final sanction letter carries the precise terms of your loan and is the document that leads directly to signing the loan agreement and subsequent disbursement.

For visa applications, always submit the final sanction letter where possible. It carries significantly more credibility with embassy officials than an in-principle letter.

► MY POV: In my experience tracking study-abroad loan cases, I find that students often accept an in-principle letter without pushing the lender for a final sanction. If you have your university admission confirmed and all documents ready, do not stop at the in-principle stage. Push for the final sanction letter immediately. It gives you stronger visa documentation and removes uncertainty from the process.

Read More: Education Loan Eligibility Criteria in India: Everything You Need to Know

Importance of the Sanction Letter: Visa and University Admission

The education loan sanction letter is the document that connects your financial backing to two critical gatekeepers: your university and the embassy of the country you plan to study in.

For University Admission

Most foreign universities require proof of funds before they confirm your enrollment. An education loan sanction letter directly addresses this requirement. It demonstrates that a regulated financial institution has evaluated your case and committed to funding your education.

The letter is particularly important for courses in countries like the USA, Canada, the UK, and Australia, where universities check financial capacity before issuing official admission documents (I-20 for USA, CAS for UK, CoE for Australia).

For Student Visa Applications

Visa authorities want evidence that you can fund your stay for the entire duration of the course without becoming a financial burden on the host country.

For a US student visa (F-1), the DS-160 application requires you to provide evidence of financial support. A final sanction letter from an Indian bank, when accompanied by bank statements and a fee demand from the university, constitutes strong financial evidence.

For UK visas, you typically need to show funds held for a consecutive 28-day period. A sanction letter alone may not satisfy this; you may need to draw down part of the loan into a savings account to meet the UK’s specific funds-in-account requirement.

For Canada and Australia, rules vary by institution and immigration category, but a final sanction letter is universally accepted as part of the financial evidence package.

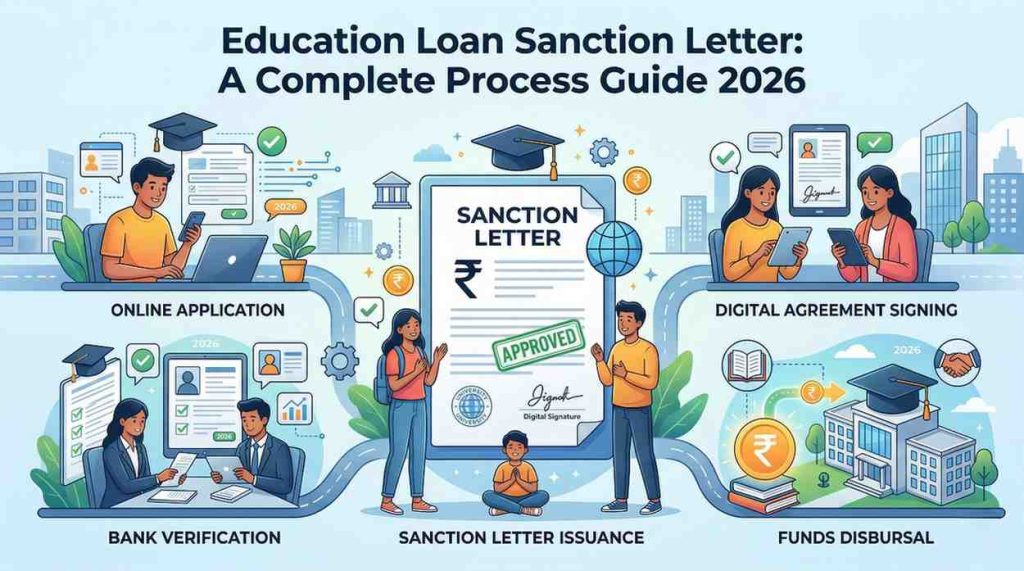

The Process: From Application to Sanction Letter

Understanding the full process helps you plan your timeline accurately, especially if you are working against a university admission deadline.

Step 1: Application Submission

You submit your loan application with complete documentation, your academic records, co-applicant’s income proof, property documents (if collateral is involved), and course admission details if available.

Step 2: Credit and Risk Assessment

The bank evaluates your co-applicant’s repayment capacity, your academic profile, the institution’s ranking and employability outcomes, and the value of any collateral pledged. This stage typically takes 7 to 21 working days depending on the lender.

Step 3: Sanction Committee Approval

Once the credit assessment clears, the file goes to the bank’s credit committee for final approval. At this point, the terms of the loan are finalised.

Step 4: Sanction Letter Issued

The bank issues the formal sanction letter with all loan terms clearly stated. This is the document you use for university and visa purposes.

Step 5: Loan Agreement Signing

Once you have your university admission and visa (or simultaneously, depending on the lender’s process), you sign the formal loan agreement. This is the legal contract between you and the lender.

Step 6: Disbursement

The bank releases funds directly to the university’s fee account (for tuition) and to your account (for living expenses), as per the disbursement schedule agreed in the loan agreement.

Sanction Letter Validity: How Long Does It Last?

This is one of the most under-explained aspects of the education loan process, and it creates real problems for students whose visa timelines slip.

Most Indian banks and NBFCs issue sanction letters valid for 3 to 6 months from the date of issuance. Some lenders extend this to 12 months for study-abroad loans where visa processing timelines are unpredictable.

If your sanction letter expires before you complete your visa process or before your course begins, you need to request a revalidation or renewal from the bank. Most lenders issue a fresh letter after a brief re-verification of your documents and co-applicant’s current income status.

Do not assume your sanction letter remains valid indefinitely. I have seen students lose admission deposits because they assumed the bank’s commitment had no expiry. Check the validity date on the first page of your letter and set a reminder 30 days before it expires.

If your co-applicant’s financial circumstances have changed significantly between the original sanction and the renewal request, the bank may revise the terms. This is rare but worth being aware of.

Sanction vs Disbursement: The Distinction Most Students Miss

This confusion is so common that I want to address it as its own section, not just a passing note.

| Parameter | Sanction | Disbursement |

|---|---|---|

| What it means | Loan has been approved | Money has been released |

| Document | Sanction letter | Disbursement advice / bank transfer |

| When it happens | After credit assessment | After loan agreement signing |

| What you can do with it | Show to university, embassy | Pay fees, fund expenses |

| Is money available? | No | Yes |

| What is required before this | Application + documents + assessment | Sanction letter + loan agreement + admission + visa |

The sanction is the bank’s promise. The disbursement is the bank’s payment. Between the two sits the loan agreement, which is the legal contract you sign after receiving the sanction letter and before money is released.

Post-Sanction Steps: What You Must Do After Receiving the Letter

Receiving the sanction letter is not the end of the process. It is the beginning of the final phase.

- Review every term in the letter carefully, particularly the interest rate type (fixed or floating), moratorium duration, and EMI amount after moratorium. If anything does not match what you were verbally told, raise it with the bank before signing anything.

- Use the letter immediately for university and visa purposes. Do not wait until after your visa is stamped to circulate this document.

- Request a physical copy with the bank’s official seal and authorised signature. Digital PDF versions are acceptable for many purposes, but some embassies and universities require a wet-signed physical copy.

- Arrange the loan agreement signing appointment. Your bank will schedule this once you have your visa or as part of the pre-visa process depending on their procedure.

- Understand the disbursement schedule. Most banks do not release the entire loan amount upfront. They disburse semester by semester or as per the university’s fee due dates. Knowing this schedule helps you plan your living expense funding.

- Maintain your co-applicant’s documents in updated form. If the bank requests fresh income documents at disbursement stage, you want to be prepared without delays.

Common Mistakes to Avoid With Your Sanction Letter

Based on the patterns I have observed in the Indian student loan space, these are the errors that cause the most serious consequences.

Confusing sanction with funds in account. Never state on a visa application that sanctioned loan funds are “available in your account.” They are not. The correct statement is “I have a sanctioned education loan of Rs. X from [Bank Name], which will be disbursed upon course commencement.”

- Submitting an in-principle letter where a final sanction letter is required, particularly for visa applications. Always clarify with the embassy which type they accept.

- Not checking the validity date and missing it. A lapsed sanction letter requires renewal and causes delays.

- Failing to read the conditions precedent section. These are the bank’s requirements before disbursement. Missing even one condition can delay your first tuition payment.

- Signing the loan agreement without understanding the prepayment penalty clause. Some lenders charge a fee if you repay the loan early. This matters if you plan to foreclose the loan after getting a job abroad.

- Assuming the sanctioned amount includes all expenses. Some banks sanction tuition only and exclude living costs. Verify the scope of coverage before finalising.

Conclusion

The education loan sanction letter is not just a piece of paper, it is the document that unlocks your university seat and your student visa. Understanding what it contains, which type to use where, and what comes after it separates students who move through the process smoothly from those who face delays at the visa counter or the admissions office.

If you have received your sanction letter, read every term carefully before signing anything. If you have not yet applied, use this guide to know exactly what you should expect your letter to contain and what to verify before accepting the terms.

For more guidance on the full education loan process in India, from application to disbursement to repayment, explore the related articles on this site.

Disclaimer: Loan terms, interest rates, and visa requirements change regularly. Always verify current conditions directly with your lender and the relevant embassy before making financial decisions.

Frequently Asked Questions

What is an education loan sanction letter?

An education loan sanction letter is an official document issued by a bank or NBFC confirming that your loan application has been approved. It states the approved loan amount, interest rate, repayment tenure, moratorium period, and the conditions that must be met before disbursement.

Is the sanction letter enough for a US student visa (F-1)?

A final sanction letter from a recognised Indian bank is accepted as financial evidence for the US F-1 visa when accompanied by supporting documents. However, the consular officer has discretion to ask for additional proof of financial capacity such as bank statements from your co-applicant.

What happens after receiving the education loan sanction letter?

After receiving the letter, you use it for university admission confirmation and visa application. Once your visa is stamped, you sign the formal loan agreement with the bank, after which the bank disburses funds as per the agreed schedule.

How long is an education loan sanction letter valid?

Most Indian banks and NBFCs issue sanction letters valid for 3 to 6 months from the date of issue. Some lenders extend validity to 12 months for study-abroad cases. If your letter expires, you can request a renewal from the bank.

What is the difference between sanction and disbursement?

Sanction means the bank has approved your loan and committed to lending you the money. Disbursement means the money has actually been transferred, either to the university’s fee account or to your account. Disbursement only happens after the loan agreement is signed following the sanction.

Can an in-principle sanction letter be used for university admission?

Yes, most universities accept an in-principle or pre-approved sanction letter for issuing an offer letter, I-20, or CAS. However, for visa purposes, a final sanction letter with all terms confirmed carries considerably more weight.

What should I do if my sanction letter has expired?

Contact your bank immediately and request a revalidation or fresh sanction letter. Bring your co-applicant’s updated income documents. The bank will re-verify the file and issue a renewed letter, usually within 5 to 10 working days.

Source and Reference:

https://studyinthestates.dhs.gov/students/prepare/financial-ability

https://www.education.gov.in/en/scholarships-education-loan-4

https://www.rbi.org.in/commonperson/English/Scripts/FAQs.aspx?Id=3372

https://www.iba.org.in/circulars/iba-model-educational-loan-scheme-for-pursuing-higher-education-in-india-andamp-abroad-2022-_1456.html

https://studyinthestates.dhs.gov/students/prepare/financial-ability

https://www.gov.uk/guidance/financial-evidence-for-student-and-child-student-route-applicants