Most Indian families paying full interest on their education loan do not know the government was supposed to cover a significant part of it.

I find this gap staggering every time I research this topic. Crores of rupees in interest subsidies go unclaimed every year across India, not because students are ineligible, but because nobody told them these schemes exist. Private loan websites skip them because there is no commission to earn. Bank relationship managers sometimes forget to mention them. Education consultants focus on admissions, not finance.

This guide changes that. I cover every central government education loan schemes in India that is active in 2026, CSIS, PM Vidyalaxmi, Dr Ambedkar, CGFSEL, plus the most significant state-level schemes, exactly who qualifies for each, what the actual benefit is in rupees, and the step-by-step process to apply.

Quick Facts: Government Education Loan Schemes 2026

| Scheme | Benefit | Max Loan | Income Limit | For Whom |

|---|---|---|---|---|

| CSIS (PM-USP) | Full interest subsidy during moratorium | Rs.10 lakh | Up to Rs.4.5 lakh/year | EWS students, domestic technical/professional courses |

| PM Vidyalaxmi | 3% interest subvention + collateral-free loan | Rs.10 lakh | Up to Rs.8 lakh/year | Students in 902 QHEIs |

| Dr Ambedkar Scheme | Full interest subsidy during moratorium | Rs.20 lakh | OBC: Rs.3 lakh; EBC: Rs.1 lakh | OBC and EBC students for overseas studies |

| CGFSEL | 75% credit guarantee, no collateral needed | Rs.7.5 lakh | Up to Rs.4.5 lakh/year | EWS students without collateral |

| Padho Pardesh | Discontinued as of 2022 | N/A | N/A | Was for minority overseas students |

| State schemes | Varies by state | Varies | Varies | State-specific eligibility |

Why Government Education Loan Schemes Matter More Than You Think

Before I walk through each scheme, it helps to understand what these schemes actually do in financial terms, because the abstract phrase “interest subsidy” understates the real impact considerably.

Take a student who borrows Rs.10 lakh at 10.5% for a 4-year engineering programme. Without a government scheme, interest accrues throughout the course and moratorium period at simple interest, adding roughly Rs.4.2 lakh to the principal before the first EMI is even due. A full interest subsidy under CSIS or PM Vidyalaxmi means the government pays that entire Rs.4.2 lakh on the student’s behalf. The student starts repayment on a clean Rs.10 lakh principal, not on Rs.14.2 lakh.

That is not a minor benefit. For a family earning Rs.3 to Rs.4 lakh a year, it is the difference between a manageable loan and a crushing one.

The central government runs four active schemes that target different student categories. They work alongside, not instead of, your bank education loan. You take the loan from a scheduled bank under the IBA Model Scheme, and the government pays the subsidy portion directly into your loan account or CBDC wallet.

► MY POV: In my research into this space, I consistently find that awareness of these schemes is highest in urban areas and among students whose parents have some financial literacy. Students from tier-2 and tier-3 cities, first-generation college-goers, and students from SC/ST/OBC communities are precisely the groups these schemes were designed for, and precisely the groups least likely to have heard of them. If you are reading this and you fall into any of those categories, read every scheme below carefully. There is a meaningful chance the government owes you money you have not claimed.

Scheme 1 — Central Sector Interest Subsidy Scheme (CSIS)

What It Is

The Department of Higher Education, Ministry of Education has been implementing the Central Sector Interest Subsidy (CSIS) Scheme since 2009. Under this scheme, interest subsidy is given during the moratorium period, that is, the course period plus one year, on education loans taken from scheduled banks under the Model Education Loan Scheme of the Indian Banks Association, for students belonging to economically weaker sections whose annual parental income is up to Rs.4.5 lakh from all sources.

In plain terms: if your family earns under Rs.4.5 lakh a year and you take a loan for a technical or professional course at an approved institution, the government pays your entire interest during your course and for one year after you graduate. You touch none of it.

Who Qualifies for CSIS?

- Indian citizen pursuing a full-time technical or professional course in India

- Annual parental income from all sources must not exceed Rs.4.5 lakh

- Loan must be from a scheduled commercial bank under the IBA Education Loan Scheme

- The institution must be NAAC-accredited, or the programme must be accredited by NBA, or the institution must be an Institution of National Importance or a Centrally Funded Technical Institution (CFTI)

- Applies only to domestic studies, not for courses abroad

- Maximum loan amount eligible for subsidy: Rs.10 lakh

What You Actually Save

On a Rs.10 lakh loan at 10.5% over a 4-year course plus 1-year moratorium, the government covers approximately Rs.4 to Rs.5.25 lakh in interest. You begin repayment on the original principal amount, not on a compound-inflated sum.

How to Apply for CSIS

Students can apply online for education loan and interest subvention under PM-Vidyalaxmi and CSIS scheme at pmvidyalaxmi.co.in. Students must register through Aadhaar for availing interest subsidy under the schemes. The subsidy amount is credited to the PM Vidyalaxmi Digital Rupee App (CBDC Wallet) of the beneficiary.

Step 1: Apply for your education loan at a scheduled bank under the IBA scheme.

Step 2: Register on the PM Vidyalaxmi portal at pmvidyalaxmi.co.in using your Aadhaar.

Step 3: Submit your income certificate, admission proof, loan sanction letter, and bank account details through the portal.

Step 4: The bank processes your subsidy claim. Canara Bank is the Nodal Bank for CSIS implementation.

Step 5: Subsidy is credited to your CBDC wallet and then transferred to your loan account.

Scheme 2 — PM Vidyalaxmi Scheme (Launched November 2024)

What It Is

PM Vidyalaxmi will build on and further enhance the scope and reach of the range of initiatives undertaken by the Government of India, supplementing the Central Sector Interest Subsidy and Credit Guarantee Fund Scheme for Education Loans. A special loan product enables collateral-free, guarantor-free education loans.

A mission mode mechanism facilitates the extension of education loans to meritorious students who get admission in the top 860 quality higher educational institutions of the nation, translating to covering more than 22 lakh students every year.

This is the newest and most significant central government education loan initiative, announced by the Cabinet in November 2024 and now active in 2026 with 902 Quality Higher Educational Institutions (QHEIs) listed on the portal.

What the PM Vidyalaxmi Scheme Offers

The scheme provides a 75% credit guarantee by the Government of India for loan amounts up to Rs.7.5 lakh irrespective of family income, a 3% interest subvention on loans up to Rs.10 lakh for students with annual family income up to Rs.8 lakh during the moratorium period, and full interest subvention to students with up to Rs.4.5 lakh annual family income under PM-USP CSIS for technical and professional courses. An additional 1% interest concession applies if interest is serviced during the study period and moratorium period.

Who Qualifies?

- Indian citizen admitted to one of the 902 QHEIs listed on the PM Vidyalaxmi portal

- For the 3% interest subvention: annual family income up to Rs.8 lakh

- For full interest subvention: annual family income up to Rs.4.5 lakh (combined with CSIS)

- No collateral or guarantor required, this is the core feature of this scheme

- Loan must be taken through the PM Vidyalaxmi portal from a participating bank

Read Me: NBFC Education Loan 2026: Top Providers, Eligibility & How to Apply in India

The 902 QHEIs List

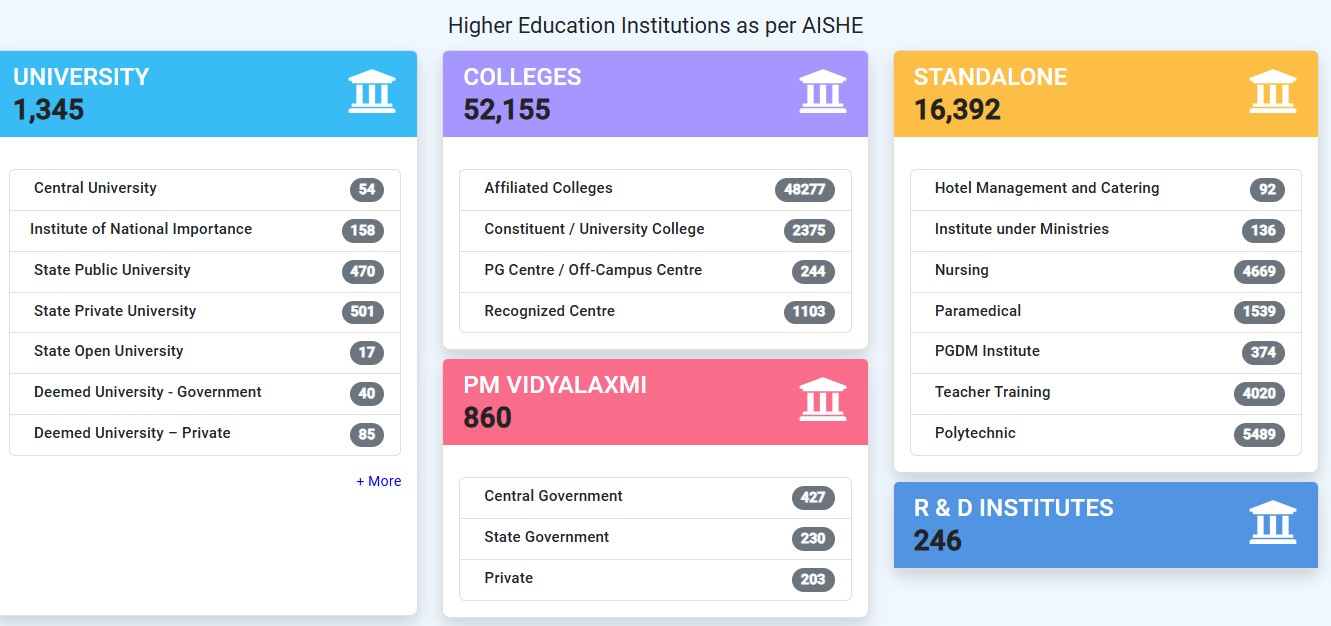

The QHEIs include IITs, IIMs, NITs, AIIMS, central universities, and other NAAC A++ or A+ institutions. The full updated list is available at dashboard.aishe.gov.in. If your target institution is on this list, PM Vidyalaxmi is the first scheme you should apply under.

How to Apply

Step 1: Visit pmvidyalaxmi.co.in and create a student account using your Aadhaar.

Step 2: Search for your institution in the QHEI list and confirm it is covered.

Step 3: Apply for the loan through the portal, it connects you to over 45 participating banks and financial institutions in one window.

Step 4: Select your preferred bank, submit documents, and apply for the interest subvention simultaneously.

Step 5: Track your application status through the portal dashboard.

► MY POV: PM Vidyalaxmi is the most meaningful expansion of government education finance support in over a decade. The key advantage most students miss is the no-collateral, no-guarantor feature combined with the 3% interest subvention. For a family earning Rs.6 to Rs.8 lakh a year, too high for full CSIS benefit but still genuinely stretched, the 3% subvention on a Rs.10 lakh loan saves approximately Rs.1.5 to Rs.2 lakh over the course and moratorium period. That is real money for a middle-income household.

Scheme 3 — Dr Ambedkar Interest Subsidy Scheme (OBC and EBC Students)

What It Is

The objective of the Dr Ambedkar scheme is to award interest subsidy to meritorious students belonging to the Other Backward Classes and Economically Backward Classes so as to provide them better opportunities for higher education abroad and enhance their employability.

This scheme is specifically for overseas studies, not domestic courses, and covers Master’s, M.Phil., and PhD programmes. It is administered by the Ministry of Social Justice and Empowerment, with Canara Bank as the Nodal Bank.

Who Qualifies?

- Must belong to the OBC (Other Backward Classes) or EBC (Economically Backward Classes) category

- For OBC candidates, annual income from all sources must not exceed Rs.3 lakh. For EBC candidates, it must not exceed Rs.1 lakh. Note: Some updated guidelines reference Rs.8 lakh for OBCs, always verify the current income ceiling with your bank at the time of application, as these figures are periodically revised.

- Must have secured admission in an approved Master’s, M.Phil., or PhD programme at a recognised foreign institution

- Must have taken an education loan from a scheduled bank under the IBA Education Loan Scheme

- Maximum loan eligible for subsidy: Rs.20 lakh. The subsidy covers the entire moratorium period, course duration plus one year, or six months after getting a job, whichever is earlier.

- 50% of the annual outlay is earmarked for girl students under this scheme.

What You Save

Full interest subsidy during moratorium on up to Rs.20 lakh. On a Rs.15 lakh loan at 11% over a 2-year Master’s programme plus 1-year moratorium, this scheme covers approximately Rs.4.95 lakh in interest, completely paid by the government.

How to Apply

The Dr Ambedkar scheme application is processed through the Nodal Bank (Canara Bank) and the National Scholarship Portal (scholarships.gov.in). You must apply alongside your education loan application at a scheduled bank. Bring your OBC/EBC caste certificate issued by a competent authority, income certificate from a state government authority, admission letter from the foreign university, and your loan sanction letter.

Scheme 4 — Credit Guarantee Fund Scheme for Education Loans (CGFSEL)

What It Is

Under the CGFSEL, the Central Government gives a guarantee for education loans availed by students without any collateral security and third-party guarantee for a maximum loan limit of Rs.7.5 lakh. The Fund provides guarantee cover to the extent of 75% of the amount in default through the National Credit Guarantee Trustee Company Ltd. (NCGTC).

CGFSEL is not an interest subsidy scheme, it is a credit guarantee. What that means in practice: when a student from an economically weaker background applies for an education loan of up to Rs.7.5 lakh without offering any collateral or guarantor, the bank is nervous about lending because it has no security. CGFSEL removes that nervousness by backing 75% of any default. The bank lends more willingly. The student gets the loan.

Who Qualifies?

- Indian citizen from economically weaker sections (annual family income up to Rs.4.5 lakh)

- Secured admission in a recognised technical or professional course in India or abroad

- Loan must be taken under the IBA Model Education Loan Scheme from a member lending institution

- No collateral required for loans up to Rs.4 lakh. For loans above Rs.4 lakh and up to Rs.7.5 lakh, some margin money or third-party guarantee may apply depending on the bank’s policy.

Interest Rate Cap

The lending institution can charge a maximum interest of 2% per annum above the base rate on education loans under the CGFSEL scheme. The lender cannot charge any margin money on CGFSEL scheme education loans for amounts up to Rs.4 lakh.

How to Apply

CGFSEL is applied for automatically through your bank when you take an education loan up to Rs.7.5 lakh under the IBA scheme. You do not apply separately. The bank handles the guarantee registration with NCGTC on your behalf. You can also apply through the Vidya Lakshmi portal at vidyalakshmi.co.in, which connects to all participating member lending institutions.

Scheme 5 — Padho Pardesh Scheme (Discontinued — Status in 2026)

I want to address this directly because several outdated articles still list Padho Pardesh as an active scheme.

Padho Pardesh, which provided interest subsidies for minority students studying abroad, has been discontinued. It was officially wound down in 2022. If any bank relationship manager or education consultant tells you to apply under Padho Pardesh in 2026, that is incorrect information.

Minority students, Muslims, Christians, Sikhs, Buddhists, Parsis, and Jains, who previously benefited from Padho Pardesh should now explore the Dr Ambedkar scheme (if they fall under OBC/EBC categories) or the PM Vidyalaxmi scheme for domestic courses.

Scheme 6 — PM Vidya Lakshmi Portal (The Single-Window Application Gateway)

The PM Vidya Lakshmi Portal, now accessible at pmvidyalaxmi.co.in, deserves its own section because it is not simply a portal. It is the gateway through which every central government education loan scheme is now accessed.

The Vidyalakshmi portal is a government-backed online platform launched in 2015 by the Department of Financial Services, Ministry of Finance, in collaboration with NSDL e-Governance. It acts as a single window for students to search, compare, and apply for education loans from over 45 banks and financial institutions.

Through a single registration on this portal, a student can apply for loans from multiple banks simultaneously, track application status in real time, access CSIS and PM Vidyalaxmi interest subvention benefits, and file grievances if a bank delays processing.

The portal’s significance increased substantially after PM Vidyalaxmi launched in November 2024. It now functions as the primary interface between meritorious students, participating banks, and the Ministry of Education’s subsidy disbursement system.

If you apply for any government education loan scheme in India in 2026, your starting point is pmvidyalaxmi.co.in.

State Government Education Loan Schemes

Beyond the central schemes, several Indian states run their own education loan subsidy programmes that are genuinely valuable but severely under-publicised.

Gujarat Government Education Loan Scheme for Abroad Studies

The Gujarat Government Education Loan for abroad studies helps financially challenged students of Gujarat to pursue overseas education. Under this student loan, economically weaker students can get a 100% subsidy on the interest rate of the loan amount. This means a qualifying Gujarat student pays back only the principal, zero interest. Eligibility is income-based and restricted to Gujarat domicile students.

Kerala Education Loan Interest Subsidy

The Kerala State Education Loan Subsidy Scheme provides partial reimbursement of interest paid on education loans for overseas study. It operates through the Kerala State Backward Classes Development Corporation and targets students from backward communities pursuing higher education abroad. The subsidy amount and eligibility criteria are updated annually, check the Kerala Social Welfare Department’s official portal for current figures.

Tamil Nadu TAMCO Scheme

Through the Tamil Nadu Minorities Economic Development Corporation (TAMCO), minority community students with a family income between Rs.1.03 lakh and Rs.6 lakh can apply for subsidised loans. Tamil Nadu also actively implements the CSIS scheme, further increasing accessibility for students.

Other Active State Schemes

Several other states, Karnataka, Rajasthan, Madhya Pradesh, Odisha, and Uttar Pradesh, run interest subvention or direct loan subsidy schemes for SC/ST students, girl students, and students from economically weaker backgrounds. These are administered through respective State Backward Classes Finance and Development Corporations and State Minority Finance Corporations. Your state’s Social Welfare Department website is the authoritative source for current scheme details.

Full Comparison Table: All Government Education Loan Schemes 2026

| Scheme | Ministry | Domestic or Abroad | Max Loan | Income Limit | Key Benefit | Apply At |

|---|---|---|---|---|---|---|

| CSIS (PM-USP) | Ministry of Education | Domestic only | Rs.10 lakh | Up to Rs.4.5 lakh/year | Full interest subsidy during moratorium | pmvidyalaxmi.co.in |

| PM Vidyalaxmi | Ministry of Education | Domestic (QHEIs) | Rs.10 lakh | Up to Rs.8 lakh/year for 3% subvention | 3% interest subvention + no collateral | pmvidyalaxmi.co.in |

| Dr Ambedkar Scheme | Ministry of Social Justice | Abroad only | Rs.20 lakh | OBC: Rs.3 lakh; EBC: Rs.1 lakh | Full interest subsidy during moratorium | scholarships.gov.in + Nodal Bank |

| CGFSEL | Ministry of Education | Both India and Abroad | Rs.7.5 lakh | Up to Rs.4.5 lakh/year | 75% credit guarantee, no collateral | vidyalakshmi.co.in + bank |

| Padho Pardesh | Discontinued | N/A | N/A | N/A | Discontinued in 2022 | N/A |

| Gujarat State Scheme | Government of Gujarat | Abroad | Varies | EWS criteria | 100% interest subsidy | State government portal |

| Kerala State Scheme | Government of Kerala | Abroad | Varies | Backward classes | Partial interest reimbursement | Kerala Social Welfare Dept |

How to Apply on the National Scholarship Portal (NSP) for Dr Ambedkar Scheme

The National Scholarship Portal at scholarships.gov.in is the application gateway for the Dr Ambedkar Interest Subsidy Scheme and several other central government education finance programmes.

Step 1: Visit scholarships.gov.in and click on New Registration.

Step 2: Register with your Aadhaar number, mobile number linked to Aadhaar, and bank account details.

Step 3: Log in and search for the Dr Ambedkar Interest Subsidy Scheme under the Ministry of Social Justice and Empowerment section.

Step 4: Fill in the application form with your personal details, caste certificate information, income certificate details, admission information, and bank loan details.

Step 5: Upload required documents, caste certificate, income certificate, admission letter from foreign university, loan sanction letter, and bank account details.

Step 6: Submit the application. Your bank’s Nodal Officer will verify and process the subsidy claim with Canara Bank.

What Others Miss: Two Overlooked Angles on Government Education Loan Schemes

The Stacking Opportunity

Most students apply for one scheme. What many do not realise is that CSIS and CGFSEL are designed to work together. A student from an EWS family can take a collateral-free loan under CGFSEL and simultaneously receive the full CSIS interest subsidy during the moratorium. The credit guarantee removes the bank’s hesitation to lend. The interest subsidy removes the student’s interest burden. Together, they make education finance genuinely accessible for families at the Rs.3 to Rs.4 lakh annual income level.

The PM Vidyalaxmi QHEIs List Is Expanding

The PM Vidyalaxmi Guidelines 2024 list 902 quality higher educational institutions, with 42 additional QHEIs recently added through a public notice. This list is not static. The Ministry of Education reviews and expands it periodically. If your target institution was not on the list 6 months ago, check again, it may have been added. The current list is always at dashboard.aishe.gov.in.

Common Mistakes When Applying for Government Education Loan Schemes

Not applying at the same time as the loan. Government scheme subsidies must be linked to your IBA loan application from the start. Trying to add a subsidy claim after disbursement begins creates complications. Apply for the scheme and the loan together.

- Submitting an income certificate that is more than 6 months old. Most schemes require a fresh income certificate issued by a competent state authority. An old certificate will delay or reject your application.

- Applying under a scheme you do not qualify for. CSIS is domestic only. Dr Ambedkar is abroad only. Confusing these wastes time and creates processing delays.

- Ignoring the CBDC wallet step under PM Vidyalaxmi. The subsidy amount is credited to the PM Vidyalaxmi Digital Rupee App (CBDC Wallet) of the beneficiary. Students must activate this app through an Aadhaar-based authentication process via OTP received on their Aadhaar-registered mobile number. Not activating the wallet means the subsidy sits unclaimed even after it is sanctioned.

- Assuming the bank will automatically notify you. Banks are supposed to inform eligible borrowers of available schemes, but this does not always happen reliably. You are responsible for knowing your eligibility and applying proactively.

- Choosing a bank that is not a member lending institution under CGFSEL or not registered with the PM Vidyalaxmi portal. Always check the portal’s list of participating banks before selecting your lender.

Key Takeaways

- Four active central government schemes exist in 2026, CSIS, PM Vidyalaxmi, Dr Ambedkar, and CGFSEL. Each targets a different student category. Check your eligibility for all four before applying.

- CSIS provides full interest subsidy during moratorium for EWS students taking domestic technical or professional courses. Maximum loan: Rs.10 lakh. Income limit: Rs.4.5 lakh/year.

- PM Vidyalaxmi (launched November 2024) provides 3% interest subvention and collateral-free loans for students admitted to 902 QHEIs including IITs, IIMs, and NITs. Income limit: Rs.8 lakh/year for subvention.

- Dr Ambedkar Scheme covers OBC and EBC students taking Master’s, M.Phil., or PhD courses abroad. Maximum subsidised loan: Rs.20 lakh. Full interest subsidy during moratorium.

- CGFSEL provides a 75% government credit guarantee on loans up to Rs.7.5 lakh for EWS students without collateral.

- Padho Pardesh has been discontinued since 2022. Do not apply.

- Apply through pmvidyalaxmi.co.in for CSIS and PM Vidyalaxmi. Apply through scholarships.gov.in for Dr Ambedkar Scheme.

- CSIS and CGFSEL can be used together, this combination gives EWS students both a collateral-free loan and zero interest during their moratorium.

Conclusion

Government education loan schemes in India represent one of the most significant but least-utilised forms of financial support available to Indian students. The CSIS, PM Vidyalaxmi, Dr Ambedkar scheme, and CGFSEL together provide interest subsidies, credit guarantees, and collateral-free loans that can save eligible students Rs.2 lakh to Rs.5 lakh or more over their loan tenure.

The only requirement is knowing they exist and applying on time.

Start at pmvidyalaxmi.co.in if you are taking a domestic education loan. Start at scholarships.gov.in if you are an OBC or EBC student heading abroad for Master’s or PhD studies. Apply for your government scheme at the same time as your bank loan, not after.

The money is there. The application process is online. The only thing standing between you and a significantly lighter loan burden is the 30 minutes it takes to register and apply.

Frequently Asked Questions

What government education loan schemes are available in India in 2026?

Four active central government schemes operate in 2026: the Central Sector Interest Subsidy Scheme (CSIS), PM Vidyalaxmi Scheme, Dr Ambedkar Interest Subsidy Scheme (OBC and EBC students for abroad studies), and the Credit Guarantee Fund Scheme for Education Loans (CGFSEL). Several state governments also run their own subsidy schemes.

Who is eligible for the CSIS education loan scheme?

Students from economically weaker sections with annual parental income up to Rs.4.5 lakh, pursuing professional or technical courses from NAAC-accredited institutions, Institutions of National Importance, or Centrally Funded Technical Institutions, and holding education loans from scheduled banks under the IBA scheme.

What is the PM Vidyalaxmi scheme and how is it different from CSIS?

PM Vidyalaxmi is a broader scheme launched in November 2024 that covers students admitted to 902 QHEIs with a 3% interest subvention for families earning up to Rs.8 lakh per year, plus collateral-free and guarantor-free loans. CSIS provides a full interest subsidy only for EWS students (income below Rs.4.5 lakh) in technical/professional courses. PM Vidyalaxmi covers a wider income band and a larger set of institutions.

Is the Dr Ambedkar scheme available for studies in India?

No. The Dr Ambedkar scheme applies only to full-time Master’s, M.Phil., and PhD courses conducted abroad. It does not apply to courses that are partly in India and partly abroad.

Can I apply for CSIS and PM Vidyalaxmi at the same time?

Yes. Students who qualify for CSIS (income below Rs.4.5 lakh, technical course, approved institution) and are also admitted to a QHEI under PM Vidyalaxmi receive both benefits, the PM Vidyalaxmi collateral-free loan structure and the full CSIS interest subsidy. Apply through pmvidyalaxmi.co.in to access both simultaneously.

Is Padho Pardesh scheme still available in 2026?

No. Padho Pardesh was discontinued in 2022. Minority students seeking overseas education finance should explore the Dr Ambedkar scheme (if OBC or EBC) or PM Vidyalaxmi for domestic courses.

Where do I apply for the Dr Ambedkar Interest Subsidy Scheme?

Applications are processed through the National Scholarship Portal at scholarships.gov.in and through the Nodal Bank (Canara Bank). You must apply alongside your IBA education loan application at a scheduled bank. Bring your caste certificate, income certificate, admission letter from the foreign institution, and loan sanction letter.

What is CGFSEL and how does it help students without collateral?

CGFSEL provides a government credit guarantee for education loans up to Rs.7.5 lakh for students from economically weaker sections. No collateral is required for loans up to Rs.4 lakh. This removes the bank’s risk in lending to students who cannot pledge property, effectively unlocking access to education finance for families with no assets to offer as security.

Disclaimer: Scheme eligibility criteria, income limits, and application processes are sourced from official government portals as of April 2026 and may be updated by the relevant ministries. Always verify current scheme details at pmvidyalaxmi.co.in, scholarships.gov.in, and education.gov.in before applying. This article does not constitute financial or legal advice.

Sources and Reference:

https://www.pmindia.gov.in/en/news_updates/cabinet-approves-pm-vidyalaxmi-scheme-to-provide-financial-support-to-meritorious-students-so-that-financial-constraints-do-not-prevent-any-youth-of-india-from-pursuing-quality-higher-education/

https://propelld.com/site/blog/vidya-lakshmi-education-loan

https://www.india.gov.in/dr-ambedkar-scheme-interest-subsidy-educational-loan-overseas-studies-obcs-ebcs

https://loansubsidy.in/aissos/

https://www.education.gov.in/en/scholarships-education-loan-4

https://www.investkraft.com/blog/vidyalakshmi-education-loan-apply-guide

https://www.shiksha.com/studyabroad/5-government-education-loan-schemes-for-students-to-study-abroad-articlepage-158077

Education Loan by Government: A Complete 2026 Guide for Students in India and Abroad