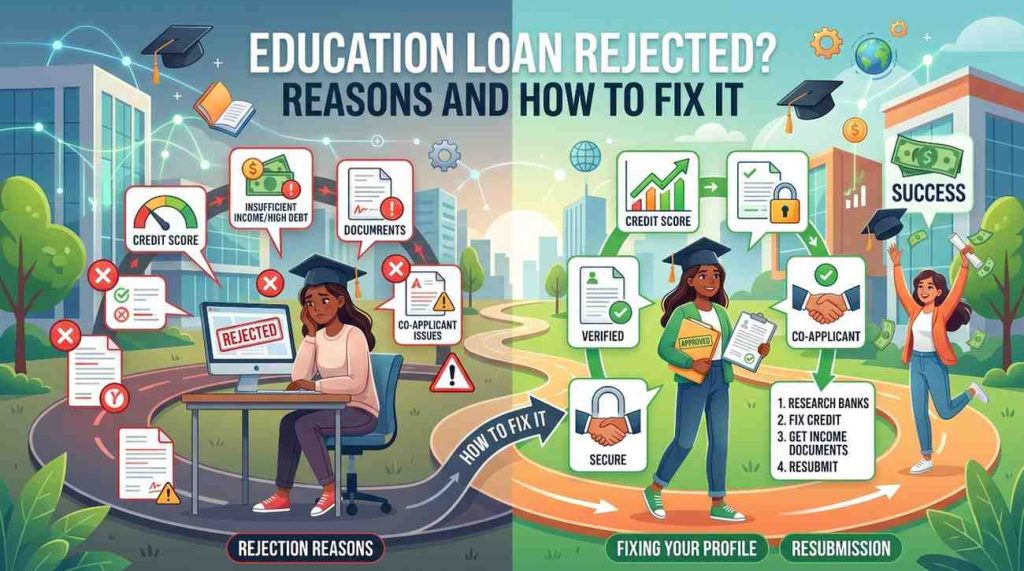

Getting a rejection letter after months of planning your future is crushing. You have the admission. You have the ambition. You have a co-applicant ready to support you. And then a bank says no.

Here is what I have found after researching hundreds of Indian student loan cases: most education loan rejections are fixable. Not all of them, and not always quickly, but the vast majority happen because of one specific, identifiable problem that has a direct solution.

The trouble is that banks rarely explain their rejection clearly. A vague “does not meet eligibility criteria” leaves students and families guessing, sometimes reapplying with the same flawed file and collecting fresh rejections that quietly damage the co-applicant’s credit score.

This guide identifies every major education loan rejection reason in India for 2026, explains exactly why each one triggers a rejection, and gives you the precise fix for each, so your next application goes in stronger, not just sooner.

Quick Facts: Education Loan Rejection in India

| Factor | Detail |

|---|---|

| Most common rejection reason | Low CIBIL score of co-applicant |

| CIBIL score minimum (unsecured loans) | 700+ for private banks and NBFCs |

| CIBIL score minimum (secured/public bank) | 650+ for government banks with collateral |

| Minimum co-applicant income (NBFCs) | Rs.30,000 to Rs.35,000/month |

| Does rejection affect your CIBIL score? | Minor temporary dip from credit inquiry only |

| Can you reapply after rejection? | Yes, after fixing the specific reason |

| How long to wait before reapplying? | Immediately (document errors); 4–6 months (CIBIL issues) |

| Agricultural land accepted as collateral? | No, by almost all major lenders |

| Does rejection affect visa application? | No, but delays caused by rejection can affect visa timelines |

Why Education Loan Rejection Is More Common Than You Think

Rejection rates for education loans, particularly for study abroad, are significantly higher than most students anticipate. Banks have tightened their underwriting considerably since a period when Non-Performing Assets in education loans reached concerning levels in the Indian banking system. The result is that lenders now scrutinise files more carefully at multiple stages.

Education loan applications are rejected due to Indian bank evaluation criteria rather than admission quality. Banks primarily assess repayment ability, not just offer letters.

This is the single most important mindset shift I want you to carry through this article. Your admission to a good university tells the bank nothing about whether your co-applicant can repay Rs.40 lakh over 10 years. The bank is not evaluating your potential, it is evaluating your family’s financial resilience. Every rejection reason in this guide connects back to that core concern.

Understanding this changes how you fix the problem. You are not trying to convince the bank that you deserve the money. You are showing the bank that the risk of default is low.

Reason 1 — Low CIBIL Score of Co-Applicant

This is the single most common education loan rejection reason across all lender types in India.

A CIBIL score above 700 to 750 for the parent or guardian is what many large lenders call “comfortable.” Repeated delays or write-offs in past loans are among the most common education loan rejection reasons even when collateral is strong.

CIBIL score of 700 and above is required for education loans without collateral. Applications with scores lower than 700 get rejected by lenders. The major reasons for low CIBIL scores are cheque bounce, delay in EMI payments, and delay in repayment of credit card bills.

For government banks with secured loans, the threshold is slightly more flexible. Government banks may accept a CIBIL score even if it is lower than 685, given it is not because of a serious issue. However, private banks lack flexibility when there are CIBIL-related issues and will mostly reject your application if the score is below 685.

Why This Triggers Rejection

The CIBIL score is the bank’s fastest indicator of repayment behaviour. A score below the threshold tells the bank that this individual has, at some point, missed payments, bounced cheques, or settled debts rather than repaying them in full. To a risk analyst, that is a red flag regardless of current income.

How to Fix It

Pull the co-applicant’s credit report, identify the specific problem, and either clear the outstanding balance or add a second guarantor with a clean credit history. Do not discover a CIBIL problem in June when your visa interview is in August.

The full fix process works like this:

- Get the co-applicant’s CIBIL report from cibil.com, check every account listed. Errors are more common than most people expect.

- Dispute any incorrect entries directly with CIBIL. Corrections take 30 to 45 days to reflect.

- Clear all outstanding credit card balances and overdue EMIs immediately. This has the fastest positive impact on the score.

- Do not apply for any new loans or credit cards during the improvement period, each new inquiry causes a small dip.

- Wait 4 to 6 months after clearing dues before reapplying, so the improved payment history has time to register in the score.

- If the co-applicant’s score cannot be improved quickly enough for your intake deadline, consider adding a second co-applicant, a working sibling, spouse, or other close relative with a clean credit history.

► MY POV: From my research into Indian education loan patterns, I find that families consistently underestimate how long CIBIL improvement takes. Clearing a debt today does not immediately raise the score, the updated status takes 45 to 60 days to appear in the bureau’s records. If your admission deadline is 6 weeks away and your co-applicant’s score is 640, improving the CIBIL score is not the right move for this intake. The right move is finding a stronger secondary co-applicant or switching to an NBFC with more flexible underwriting criteria.

Read More: Government Education Loan Schemes in India 2026: Complete List and How to Apply

Reason 2 — Insufficient Co-Applicant Income

Even with a good CIBIL score, a co-applicant whose income is too low to service the projected EMI will trigger a rejection.

Lenders generally calculate the FOIR (Fixed Obligation to Income Ratio), and the co-borrower must submit salary proof and ITR showing a minimum monthly earning of Rs.30,000 to Rs.35,000 for education loans from private banks or NBFCs.

The FOIR calculation works as follows: if a co-applicant earns Rs.50,000 per month but already pays Rs.25,000 in home loan EMIs and Rs.8,000 in car loan EMIs, their existing obligations consume 66% of income. A bank approving a new education loan EMI on top of that carries high risk, the co-applicant would have almost no financial buffer. Most banks cap FOIR at 50 to 60% of monthly income.

How to Fix It

Add a second co-applicant. Most lenders accept joint co-applicants, and the combined income of both is considered for FOIR calculations. A working sibling or spouse with no existing loan obligations can dramatically improve the profile.

Request a lower loan amount. If the issue is borderline income versus EMI, reducing the loan amount brings the projected EMI into an acceptable FOIR range. You can self-fund part of the tuition through savings, scholarships, or on-campus employment income.

Approach an NBFC. The income requirement is flexible depending on lenders and factors like course, country, CIBIL score, etc. Some platforms have negotiated with lenders for co-applicants with slightly lower incomes. NBFCs typically use more holistic underwriting that weighs academic profile and university employability data alongside income.

[IMAGE: Co-applicant income calculation FOIR education loan India | ALT TEXT: co-applicant income requirement education loan rejection fix India]

Reason 3 — Institution Not on the Bank’s Approved List

This rejection catches students off guard because they assume any accredited university automatically qualifies.

For instance, SBI’s Global Ed-Vantage and Bank of Baroda’s collateral rules for study abroad loans have lists of premier institutions and eligible programmes. If your admission is to a very new or unaccredited college, your application can be perfectly documented and still get declined.

Public sector banks like SBI and Bank of Baroda maintain internal approved institution lists, particularly for their higher loan amounts and collateral-free variants. Private banks like Axis Bank and ICICI Bank categorise institutions into tiers — A1, A2, and so on — and the loan terms, including whether margin money is required, depend on which tier your university falls into.

Banks are more likely to reject your application even when you have the required CIBIL score for an education loan if the college is not well recognised. You will not be able to secure a loan if the college has a poor placement record either.

How to Fix It

Check the bank’s approved list before applying. For SBI, you can request the current list from the branch. For NBFCs, ask the relationship manager explicitly whether your target university is on their eligible institution list.

Switch lenders. NBFCs and international lenders have broader institution coverage than public sector banks. NBFCs often have more flexible eligibility criteria, especially for high-cost international programmes. If SBI declines because your university is not on their list, HDFC Credila or Avanse may approve the same profile without hesitation.

Provide supplementary documentation. If the institution is relatively new but accredited and has strong placement data, submit QS or Times Higher Education ranking documentation, placement reports, and any industry recognition alongside your application. Some bank managers will escalate borderline cases when supported by evidence.

Reason 4 — Course Not Classified as Eligible

Related to but distinct from institution eligibility, course eligibility is a separate assessment that many students overlook.

Banks classify courses by employability potential. STEM courses, medical programmes, engineering, MBA, and law degrees carry the strongest approval probability because post-graduation income projections are reliable. Vocational programmes, arts, music, and niche humanities courses face tighter scrutiny because lenders find it harder to model repayment capacity from those career paths.

Lenders assess the potential job prospects and earning capacity of the student after completing their education. Courses with low employment rates or institutions with poor placement records can be a cause for rejection

For study abroad loans specifically, non-STEM MS programmes, fine arts degrees, and communication courses at mid-ranked foreign universities face the highest rejection risk when applied to conservative public sector banks.

How to Fix It

Apply to NBFCs or international lenders first for non-STEM programmes. Credila and Avanse use more sophisticated employability modelling. International lenders like Prodigy Finance focus heavily on the university’s career outcomes data rather than the course category.

Strengthen your application narrative. If your course is non-traditional, attach documentation showing industry demand, starting salary data from graduate surveys, and a clear career plan. While banks are primarily quantitative in their assessment, a well-documented case reduces the probability of an outright rejection.

Consider whether a GRE, GMAT, or work experience angle helps. For applications to creative or non-STEM programmes abroad, strong GRE scores and relevant work experience demonstrate future earning potential more concretely.

Reason 5 — Incomplete or Incorrect Documentation

Inadequate documentation ranks as one of the primary causes for the denial of education loans. The proper completion of documentation is a critical aspect of securing an overseas education loan, particularly in the case of collateral-based loans offered by government banks.

Documentation errors range from minor (a mismatch in name spelling between Aadhaar and PAN) to serious (missing property documents from 30+ years ago). In secured loan applications, the collateral documentation chain is especially demanding. Common causes include attaching agricultural land as collateral, land that falls under Gram Panchayat’s jurisdiction, students attaching disputed property, not submitting past sales deeds if the property has been owned for less than 30 years, and others.

Complete Documents Checklist — What Banks Verify

Student documents:

- Aadhaar and PAN Card (names must match exactly across all documents)

- Class 10, 12, and graduation marksheets and passing certificates

- GRE / GMAT / IELTS / TOEFL scorecards

- University admission or offer letter (must be unconditional or clearly conditional on financial proof only)

- University fee structure and Cost of Attendance breakdown

- Gap year explanation letter (if applicable — on Rs.100 stamp paper)

Co-applicant documents:

- PAN Card and Aadhaar Card

- Last 3 months’ salary slips (salaried) or 2 years’ ITR with CA computation (self-employed)

- 6 months’ bank statements (salary account)

- Form 16 or latest Income Tax Returns

- Proof of any existing loans (home loan statement, car loan statement)

Collateral documents (for secured loans):

- Original sale deed and all previous sale deeds (title chain for 30 years minimum)

- Property tax receipts (latest paid receipt)

- Encumbrance certificate from sub-registrar’s office

- Approved building plan and occupancy certificate

- Property insurance policy

- NOC from housing society (if applicable)

How to Fix It

Documentation rejection is the most straightforward to fix. Request the specific list of missing or incorrect documents from the bank in writing. Correct and resubmit. For property documents, engage a local property lawyer to compile the full title chain before your next application. Reapplication after a clean document submission can happen within days.

One important caution: never submit altered or fabricated documents. Some reasons for rejection include submission of fake documents. This results in permanent blacklisting by lenders and potential legal consequences, a far worse outcome than a temporary rejection.

Reason 6 — Collateral Valuation Shortfall or Wrong Property Type

For secured loans above Rs.7.5 lakh, collateral is central to the approval decision. Two distinct problems cause rejection here: the property is the wrong type, or the bank’s valuation comes in lower than the loan amount requires.

Most rejected collateral files are not about having no property. They are about the wrong kind of property for that lender. Agricultural land is usually a hard no for almost all lenders in India. SBI’s Global Ed-Vantage specifies that acceptable security is non-agricultural land, flat, building, or approved liquid assets. For many Indian families, the first big education loan rejection is due to collateral, they have plenty of land but not the kind banks can safely enforce under SARFAESI.

When a property valuation shortfall occurs, the bank’s valuation comes in lower than expected and no longer covers 100% of the loan amount.

How to Fix It

For wrong property type: Explore liquid collateral alternatives. Fixed Deposits, LIC insurance policies, government bonds, and shares are accepted by many lenders as either primary or supplementary collateral. NBFCs like Avanse accept liquid assets such as insurance policies as collateral. An FD of Rs.15 lakh pledged alongside agricultural land can bridge the gap that agricultural land alone cannot.

For valuation shortfall: Request a second independent valuation if you believe the bank’s figure is below market rate. Alternatively, offer additional liquid security (an FD or LIC policy) to bridge the gap between the valuation and the required loan coverage, or reduce the requested loan amount to align with the property’s assessed value.

For disputed or co-owned property: Resolve the ownership issue before applying. If even one key co-owner is clearly against it or unreachable, an NRI or estranged family member, choose a different asset. A bank will never accept property with contested ownership as collateral.

[IMAGE: Property documents checklist education loan collateral India | ALT TEXT: collateral property documents education loan rejection fix India]

Reason 7 — Previous Loan Default by Co-Applicant

A co-applicant who has previously defaulted on a loan, settled a debt for less than the outstanding amount, or had a loan written off as an NPA (Non-Performing Asset) presents a serious problem that goes beyond a low CIBIL score.

Having a loan settlement in the past has been the cause of education loan rejection in the case of a huge number of loan applicants. Loan settlement is treated as a serious financial offence by banks.

The reason this is more severe than a low score: a settled loan tells the bank that this individual has already demonstrated willingness to walk away from a debt commitment. That is categorically different from someone who missed payments due to temporary financial hardship but ultimately repaid.

How to Fix It

A settled or written-off loan on the co-applicant’s record is the hardest rejection reason to fix quickly. The options are:

Replace the co-applicant entirely. If the primary co-applicant (typically a parent) has a default or settlement history, the strongest fix is identifying a different co-applicant, a working sibling, spouse, or other financially stable close relative, whose credit history is clean. Most lenders require the co-applicant to be a blood relative, but policies vary between lenders.

Apply to international lenders. Prodigy Finance and MPOWER Financing do not rely on co-applicant credit histories — they assess the student’s academic profile and the university’s employment outcomes. For students applying to their eligible partner universities, these lenders offer a genuine path around co-applicant default issues.

Wait and attempt rehabilitation. For the long-term record, a co-applicant can attempt to negotiate with the original lender to formally close the settled account and regularise the credit history, though this is complex and not always possible.

Read More: Vidya Lakshmi Portal: How to Apply for a Govt Education Loan in 2026 (Step-by-Step)

What to Do Immediately After Receiving a Rejection

The 48 hours after a rejection are critical. Most students either do nothing (frozen by the shock) or immediately fire off applications to multiple banks (which creates fresh credit inquiries and compounds the problem).

Here is the right sequence:

Step 1 — Get the rejection reason in writing. SBI branches must give you a written reason for rejection. All regulated lenders in India are required to communicate the reason. If the branch officer gives you a vague verbal explanation, request a formal written rejection note. You cannot fix a problem you cannot name.

Step 2 — Do not reapply immediately with the same file. A repeat application with no changes will likely be declined, which could jeopardise your seat at the university. Each application also creates a hard inquiry on the co-applicant’s credit report.

Step 3 — Identify whether the issue is fixable before your deadline. CIBIL problems need 4 to 6 months. Documentation errors need days. Collateral issues need weeks. Match the fix timeline to your intake deadline and decide whether to fix and reapply for this intake or plan for the next one.

Step 4 — Approach a different lender type. An SBI or Bank of Baroda rejection can be because of wrong or incomplete collateral papers. An Axis Bank or ICICI Bank rejection can be because of the chosen college or university. An HDFC Credila, InCred, or Avanse rejection can be because of the co-applicant profile or CIBIL score. Different lenders fail at different points. Knowing which lender type typically struggles with your specific issue helps you target the right alternative.

Step 5 — File a grievance if the rejection seems unjustified. If you believe the rejection was arbitrary or procedurally incorrect, you can approach the bank’s internal grievance redressal mechanism and, if unresolved, file a complaint with the RBI Banking Ombudsman at cms.rbi.org.in.

How Long to Wait Before Reapplying

This is one of the most searched questions after a rejection, and the answer varies entirely by the rejection reason.

| Rejection Reason | Minimum Wait Before Reapplying |

|---|---|

| Incomplete or incorrect documentation | Immediately after correcting documents |

| Wrong collateral type or valuation shortfall | 2 to 4 weeks (once alternate collateral arranged) |

| Co-applicant income too low | Once second co-applicant is confirmed |

| Low CIBIL score | 4 to 6 months after clearing dues |

| Loan settlement or default history | 6 to 12 months minimum; or switch co-applicant |

| Institution not on approved list | Immediately at a different lender |

| Course eligibility issue | Immediately at a more flexible NBFC or international lender |

One important rule: Avoid multiple loan applications simultaneously. Each loan inquiry can further reduce your CIBIL score. Wait at least 6 months before reapplying if the issue is credit-related. For non-credit issues like documentation or institution eligibility, you can approach a new lender immediately.

What Others Miss: Two Rejection Causes That Rarely Get Mentioned

Being a Guarantor on a Defaulter’s Loan

One reason for rejection is serving as a guarantor to a defaulter. If your co-applicant signed as a guarantor on someone else’s loan years ago, a friend, a relative, and that person defaulted, your co-applicant now carries that default liability on their credit record. They may not even be aware of it. Pull the co-applicant’s full CIBIL report and check every liability, not just accounts they opened themselves.

Multiple Loan Inquiries in a Short Period

When a student applies to three banks simultaneously in a panic after the first rejection, each application generates a hard credit inquiry on the co-applicant’s record. Multiple hard inquiries within a short window signal credit-seeking behaviour to lenders, a flag that can itself cause a rejection even if the underlying profile is borderline acceptable. Multiple applications can create trust issues and a credit score impact. Apply sequentially, not simultaneously, and fix the root cause between applications.

Common Mistakes After Getting Rejected

Reapplying to the same lender with the same file. Banks record previous applications. A file that was rejected once returns to the same credit committee with its rejection history attached. Unless you have materially changed something, a new co-applicant, cleared CIBIL, fresh collateral, the outcome will be identical.

- Assuming rejection at one bank means no bank will approve. Different lenders have different criteria. A public sector bank rejection on collateral grounds does not mean an NBFC will decline the same profile.

- Not telling your university about the delay. Most universities have provisions for extending financial documentation deadlines by a few weeks for students facing genuine loan processing challenges. Contact the international admissions office proactively rather than silently missing a deadline.

- Giving up on the intake entirely. Most rejections are fixable. Low CIBIL can be improved in 4 to 6 months. No collateral means applying to lenders like Prodigy Finance. Weak academics can be addressed with a stronger SOP focused on career outcomes.

Key Takeaways

- The most common education loan rejection reason in India is a low CIBIL score of the co-applicant, below 700 for unsecured loans, below 650 to 685 for secured loans at public banks.

- Insufficient co-applicant income is the second most common cause. The FOIR (Fixed Obligation to Income Ratio) must stay within 50 to 60% after adding the projected education loan EMI.

- Institution and course eligibility are lender-specific. An institution rejected by SBI may be fully approved by Credila or Avanse. Check before applying, not after.

- Agricultural land, disputed property, or a property owned for less than 30 years without a complete title chain will cause collateral-based rejection across almost all major lenders.

- Previous loan default or settlement on the co-applicant’s record is the hardest to fix quickly. Replacing the co-applicant or switching to international lenders is often the faster path.

- After rejection, get the reason in writing, fix the specific issue, and reapply at the appropriate time. Do not fire multiple simultaneous applications, this damages the co-applicant’s CIBIL further.

- Rejection at one bank is not a life sentence. Different lender types fail on different criteria, match your profile to the right lender type before reapplying.

Read More: Best Education Loan Interest Rates in India 2026: Complete Guide

Conclusion

An education loan rejection is a problem, not a verdict. Every reason listed in this guide, low CIBIL, insufficient income, wrong collateral, incomplete documents, institution eligibility, has a direct, actionable fix. The difference between students who successfully fund their education and students who do not is rarely eligibility. It is almost always whether they identified the right problem and applied the right solution before their intake deadline.

Start by getting the rejection reason in writing. Then match the fix to your timeline. If your deadline is weeks away, focus on what can be changed fast, a second co-applicant, a different lender, better documentation. If you have months, work on the CIBIL improvement or the collateral restructuring that opens the doors to better loan terms.

The loan is out there. The path to it just needs one more clear step.

Frequently Asked Questions

Why was my education loan rejected?

The most common reasons are a low CIBIL score of the co-applicant (below 700 for unsecured loans), insufficient co-applicant income, the target institution not being on the bank’s approved list, incomplete documentation, collateral valuation shortfall, or a previous loan default or settlement on the co-applicant’s credit record.

Can I reapply for an education loan after rejection?

Yes. Most rejections are fixable. For example, if it was a problem with the co-applicant, applicant, collateral, or loan amount, take steps to resolve the specific issue and reapply or approach a different lender. Reapplying without fixing the root cause will almost certainly produce the same outcome.

Does education loan rejection affect my CIBIL score?

The rejection itself does not lower your CIBIL score. However, the credit inquiry made when you applied creates a small, temporary dip. Multiple applications within a short period create multiple inquiries, which can meaningfully affect the score.

How long should I wait before reapplying after rejection?

It depends on the reason. Documentation errors can be corrected and resubmitted within days. CIBIL-related rejections require 4 to 6 months of credit improvement work before reapplying. Collateral and income issues can be addressed in 2 to 4 weeks if alternate solutions are available.

My co-applicant’s CIBIL score is low, what can I do?

Clear all overdue credit card balances and EMIs immediately. Dispute any errors on the credit report at cibil.com. Wait 4 to 6 months for the improvement to reflect. If your intake deadline does not allow this, add a second co-applicant with a clean credit history, or apply to NBFCs that have more flexible credit thresholds.

Can I get an education loan if the bank rejected me due to the institution not being on their list? Yes. Different lenders maintain different institution lists. An SBI rejection on this ground does not mean HDFC Credila, Avanse, or international lenders like Prodigy Finance will decline the same profile. Switch lender types rather than reapplying to the same bank.

Does rejecting affect my visa application?

The rejection itself does not affect your visa outcome. However, delays caused by the rejection, missed financial documentation deadlines, delayed sanction letter, can push back your visa application timeline. Inform your university proactively if a loan delay is affecting your visa documentation.

Disclaimer: Eligibility criteria, CIBIL score thresholds, income requirements, and lender policies are sourced from official bank communications and verified third-party research as of April 2026. These figures change periodically, always verify directly with your lender before applying. This article does not constitute financial advice.