Most students spend 3 to 4 weeks on a process that can take 10 days if you know exactly what to do.

I have tracked the education loan application process across dozens of Indian families, and the pattern is consistent: delays almost never happen because of eligibility problems. They happen because students start late, gather the wrong documents, approach the wrong lender for their profile, or miss a step in the government portal process that holds everything up.

This guide covers the complete education loan application process in India for 2026, from confirming your eligibility and choosing your lender, to submitting your application, receiving your sanction letter, signing the loan agreement, and understanding exactly how disbursement works. Every step is sequenced, every document is listed, and every timeline is realistic.

Key Takeaways

- Start the education loan application process at least 8 weeks before your first fee payment deadline. Public banks take 15 to 25 working days; NBFCs take 4 to 7 working days for a complete file.

- Pull your co-applicant’s CIBIL report before applying. A score below 700 needs 4 to 6 months to improve, discover this problem before your application, not during it.

- The PM Vidya Lakshmi portal at pmvidyalaxmi.co.in allows you to apply to up to three banks simultaneously with one Common Education Loan Application Form (CELAF), track application status in real time, and access government interest subsidies.

- Choose your lender based on your profile: public banks for low rates and secured loans; NBFCs for speed, flexibility, and large unsecured amounts; direct NBFC applications for tight timelines.

- The sanction letter is used for university admission confirmation and visa applications, review every term before accepting. The loan agreement signing follows the sanction and precedes disbursement.

- Tuition fees are disbursed directly to the institution, not to you. Submit fee demand notices to your bank at least 10 working days before your institution’s fee payment deadline.

- If eligible for CSIS or PM Vidyalaxmi interest subvention, apply through the portal after disbursement and activate the PM Vidyalaxmi Digital Rupee App to receive the subsidy.

Before You Begin: Pre-Application Checklist

Before you walk into a bank or open the Vidya Lakshmi portal, five things must be in place. Missing any of them at the start adds days or weeks to your timeline.

- Confirmed admission letter from your institution — not a conditional offer, not a waitlist acknowledgement. Banks require a firm admission before processing any application seriously.

- Co-applicant identified and briefed — your co-applicant (parent, guardian, or spouse) needs to be present for parts of the process and must have their income documents ready.

- Co-applicant’s CIBIL score pulled — get this from cibil.com before approaching any bank. A score below 700 needs to be addressed before you apply, not discovered mid-process.

- Estimated cost of attendance from your institution — the total figure covering tuition, accommodation, books, travel, and living costs. This is what determines your loan amount.

- Clarity on whether you need collateral — loans above Rs.7.5 lakh typically require collateral for public banks. If you have property, have its ownership documents accessible.

Quick Reference: Education Loan Application Timeline

| Stage | Time Required | Key Action |

|---|---|---|

| Pre-application prep | 2 to 4 weeks | CIBIL check, document gathering, lender research |

| Loan application submission | 1 to 2 days | Online via portal or in-branch |

| Credit assessment and bank processing | 7 to 25 working days | Bank reviews file, may request additional documents |

| Sanction letter issued | 1 to 2 days after approval | Review and accept loan terms |

| Loan agreement signing | 1 day | Sign at bank branch |

| First disbursement | 3 to 7 days after agreement | Direct to university or student account |

| Total: Application to first disbursement | 3 to 6 weeks | Start minimum 8 weeks before first fee deadline |

Step 1 — Confirm Your Eligibility

Before choosing a lender, verify that your profile meets the standard eligibility criteria that all Indian banks assess.

Basic Eligibility Requirements

- Nationality: Indian citizen. OCI cardholders are also eligible under updated 2025 guidelines.

- Age: Typically 18 to 35 years at the time of application. Some lenders extend to 45 years for PhD or executive education.

- Academic qualification: Minimum 50 to 60% in Class 12 (relaxation for reserved categories). For postgraduate loans, undergraduate degree with adequate marks.

- Course: Full-time professional or technical programmes, engineering, medicine, management, law, architecture, and similar. Graduation, postgraduation, and PhD courses are covered.

- Institution: Must be recognised by UGC, AICTE, ICMR, or equivalent authority. For abroad loans, the institution must appear on the lender’s approved or eligible list.

- Admission basis: Admission through merit, entrance examination, or national-level counselling. Management quota admissions face tighter scrutiny.

Co-Applicant Eligibility

A co-applicant is mandatory for most education loans because students typically have no income history. The co-applicant is jointly responsible for repayment.

- Must be a close blood relative, parent, guardian, or spouse is preferred. Some lenders accept siblings with lender approval.

- Must have a stable income (salaried or self-employed)

- Minimum CIBIL score: 700+ for private banks and NBFCs; 650+ for secured loans at public banks

- Minimum monthly income: Rs.30,000 to Rs.35,000 for unsecured loans at NBFCs

Step 2 — Choose the Right Lender for Your Profile

This is the step most students rush or skip entirely, and it creates the most avoidable problems. Choosing the wrong lender for your specific profile wastes weeks and generates unnecessary credit inquiries.

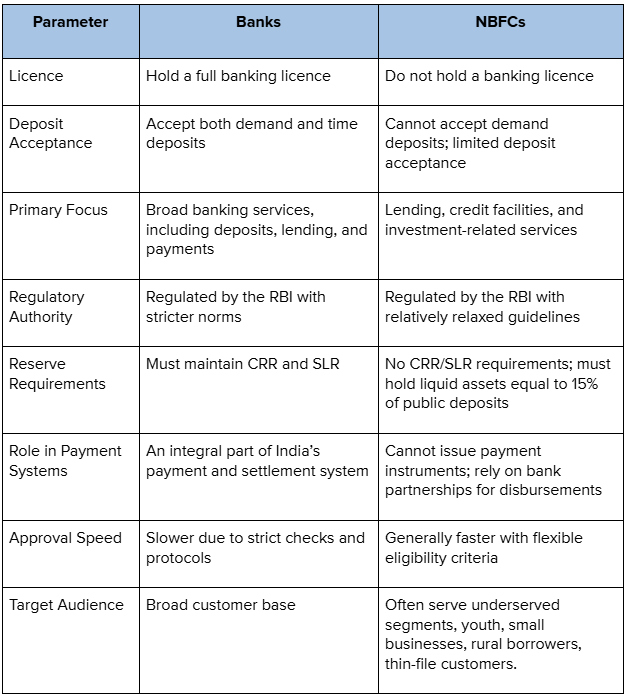

Public Sector Banks — Best for Low Interest, Secured Loans

Public banks (SBI, Bank of Baroda, Canara Bank, PNB) offer the lowest interest rates, longest repayment tenures (up to 15 years), and the highest credibility at visa counters. Their limitations are slower processing (15 to 25 working days) and stricter institution and collateral requirements.

Choose a public bank if: You have property to offer as collateral, your co-applicant has a clean credit history, you are targeting a widely recognised institution, and your loan amount is above Rs.10 lakh.

Private Sector Banks — Best for Mid-Range Profiles

Private banks (HDFC Bank, Axis Bank, ICICI Bank) sit between public banks and NBFCs in terms of rate, speed, and flexibility. Processing times run 7 to 10 working days. They categorise institutions into tiers, their best rates and collateral-free options apply only to their top-tier institutions.

Choose a private bank if: Your institution falls under their A1 or premier category, you want faster processing than a public bank, and your co-applicant has a strong financial profile.

NBFCs — Best for Speed, Flexibility, and Higher Unsecured Amounts

NBFCs (HDFC Credila, Avanse, Auxilo, InCred) process applications in 4 to 7 working days, have broader institution coverage, and offer collateral-free loans up to Rs.75 lakh to Rs.1.20 crore for strong profiles. Their interest rates are typically 1 to 3% higher than public banks.

Choose an NBFC if: You need fast processing for a visa deadline, your institution is not on a public bank’s approved list, you need a large collateral-free loan, or your profile was borderline for a public bank.

The Decision Framework

| Profile | Recommended Lender |

|---|---|

| Domestic loan under Rs.10 lakh, EWS family | Public bank + PM Vidyalaxmi portal (CSIS subsidy) |

| Domestic loan Rs.10 to Rs.30 lakh, with collateral | SBI or Bank of Baroda |

| Abroad loan, strong co-applicant, collateral available | SBI Global Ed-Vantage |

| Abroad loan, large unsecured needed (Rs.40 lakh+) | HDFC Credila or Avanse |

| Tight visa deadline (under 3 weeks for sanction) | NBFC (Credila, Avanse) |

| Profile rejected by public bank | NBFC or international lender |

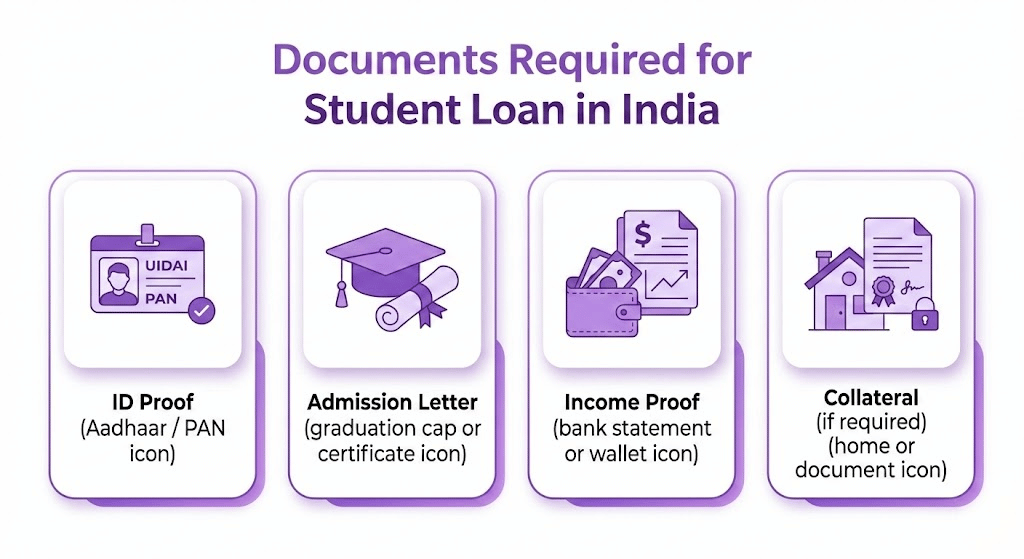

Step 3 — Gather Your Documents (Full Checklist)

Complete documents submitted upfront cut processing time by days. Incomplete files are the most common reason for “on hold” status on the Vidya Lakshmi portal and in bank branches.

Student Documents

- Aadhaar Card (must match name on all other documents exactly)

- PAN Card

- Passport (valid, minimum 6 months beyond programme end)

- Class 10 marksheet and passing certificate

- Class 12 marksheet and passing certificate

- Graduation marksheets and degree certificate (for PG loans)

- GRE / GMAT / IELTS / TOEFL score reports (for abroad loans)

- University admission or offer letter (unconditional preferred; conditional accepted for in-principle sanction)

- University fee structure and Cost of Attendance (CoA) breakdown

- Gap year explanation letter (if applicable, written on Rs.100 stamp paper)

Co-Applicant Documents

- Aadhaar Card and PAN Card

- Passport or Voter ID

- Latest 3 months’ salary slips (salaried employees)

- Form 16 or Income Tax Returns for last 2 years (both salaried and self-employed)

- 6 months’ bank statements of the salary credit account

- Proof of current employment — appointment letter or employee ID

- For self-employed: 2 years’ ITR with computation, CA-certified audited accounts, 12 months’ business account statements

- Details of any existing loans, home loan statement, car loan statement

Collateral Documents (For Secured Loans Above Rs.7.5 Lakh)

- Original sale deed and all previous sale deeds (property ownership chain for minimum 30 years)

- Property tax receipts (latest paid)

- Encumbrance certificate from sub-registrar’s office (typically for last 15 years)

- Approved building plan from the local authority

- Occupancy certificate (for constructed buildings)

- Property insurance policy

- NOC from housing society (if applicable)

- Bank-approved valuation report

For liquid collateral (FD, LIC, government bonds), bring the original certificates with nomination details.

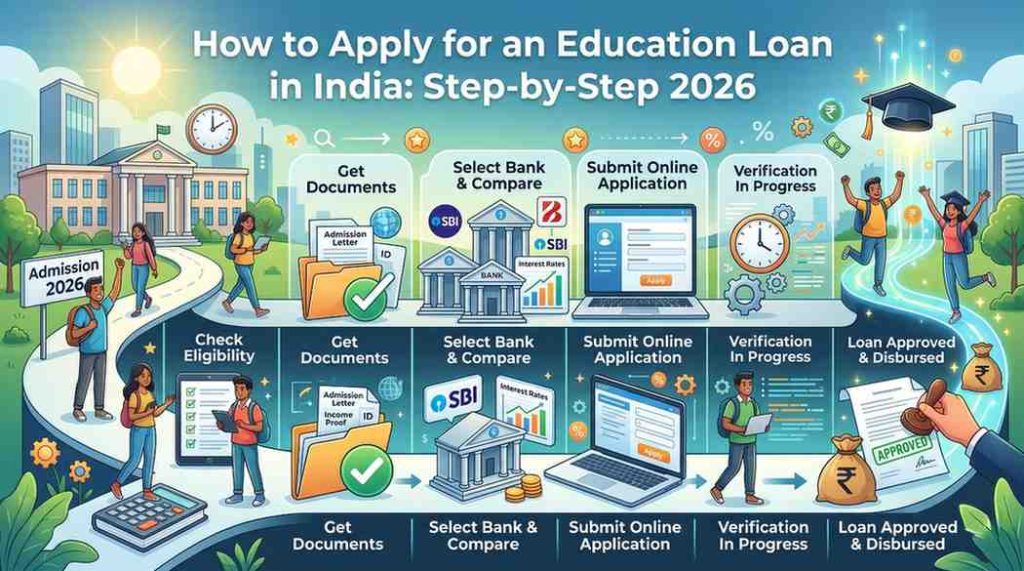

Step 4 — Apply Online or In-Branch

In 2026, you have two primary application paths: the PM Vidya Lakshmi portal for a centralised multi-bank application, or a direct application to a specific lender.

Path A — PM Vidya Lakshmi Portal (Recommended for Most Students)

The PM Vidya Lakshmi portal serves as a consolidated interactive window. Students may submit loan requests to multiple banks simultaneously. As of July 2025, the portal has successfully incorporated 48 banks including public, private, and cooperative sectors.

Through the portal, applicants can fill out one Common Education Loan Application Form (CELAF) and submit it to multiple lenders simultaneously, track application status, and apply for interest subvention under government schemes.

How to apply on PM Vidya Lakshmi portal:

Step 1: Visit pmvidyalaxmi.co.in and click “Register.”

Step 2: Fill in your name (exactly as on your Class 10 marksheet), mobile number, and email ID. Confirm registration via the link sent to your email. The link is valid for 24 hours.

Step 3: Log in and complete the Common Education Loan Application Form (CELAF). Fill every section accurately, name, course details, institution, loan amount, co-applicant details. Save the draft regularly as the session expires after 15 minutes.

Step 4: Upload your documents in the specified categories, student KYC, academic records, admission proof, co-applicant income proof, and collateral documents if applicable.

A student can apply to a maximum of three banks through Vidya Lakshmi portal using the CELAF. Multiple accounts are not allowed, a student can register only once.

Step 5: Select up to three banks from the 48 listed lenders. Compare interest rates, maximum loan amounts, and collateral requirements before selecting. You are not limited to one application, submitting to two or three banks simultaneously improves your chances without damaging your credit profile (the portal makes a soft inquiry, not multiple hard inquiries).

Step 6: Submit. Your dashboard now shows the application status for each bank in real time.

Important: If you are eligible for government interest subsidies (CSIS or PM Vidyalaxmi), apply for them through the portal simultaneously. After your education loan has been sanctioned and disbursed, log in to the PM Vidya Lakshmi website, select “Apply for Interest Subvention,” and upload your income certificate.

Path B — Direct Application to a Specific Lender

If you have already identified your preferred lender, SBI for the lowest rate, HDFC Credila for speed, Avanse for a large unsecured loan, you can apply directly through their website or branch.

Online direct application: Visit the lender’s official website, navigate to the Education Loan section, and complete the digital application form. Most NBFCs offer in-principle approval within 24 to 48 hours of a complete online submission.

Branch application (public banks): For SBI and other public banks, visit the home branch or the nearest branch with a dedicated education loan desk. Bring your complete document set. The branch officer creates your loan file and initiates the credit assessment.

Which path is better? The Vidya Lakshmi portal works best for students who want to compare multiple lenders and access government subsidies simultaneously. Direct applications work better when you have a specific lender in mind and want the fastest possible processing.

► MY POV: From my research, I find that students who apply through the Vidya Lakshmi portal and simultaneously walk into the physical branch of their preferred bank get the best of both worlds — the portal gives them the digital paper trail and subsidy access, while the branch relationship speeds up the actual processing. Banks tend to prioritise files when a student physically follows up. The portal submission alone, without any branch contact, can sit unattended for days.

Step 5 — Credit Assessment and Bank Verification

Once your application is submitted, the bank begins its internal credit assessment. This is where most of the waiting happens.

The bank’s credit team evaluates several factors simultaneously:

Co-applicant creditworthiness: CIBIL score, income stability, existing loan obligations, and Fixed Obligation to Income Ratio (FOIR). Most banks require FOIR to remain under 50 to 60% after adding the projected education loan EMI.

Student academic profile: Marks, institution ranking, course employability, and standardised test scores where applicable.

Loan-to-value ratio for collateral: For secured loans, a bank-approved valuer assesses the property. The valuation must support at least 100% of the requested loan amount for most lenders.

Institution and course verification: The bank confirms that your institution is recognised and the course is on their eligible list.

During this stage, the bank may call the co-applicant for clarifications or request additional documents. If the bank requires some further information or documents, the application status is marked “on hold” with the requirement indicated in the Remarks column on the portal dashboard. Respond to these requests within 2 to 3 working days — delays at this stage are almost always caused by students or co-applicants not responding promptly to bank queries.

Processing timelines by lender type:

For loans up to Rs.7.5 lakh, banks typically process applications within 15 days. For larger loan amounts, especially for studying abroad, the processing time may extend to 30 days. NBFCs process complete files in 4 to 7 working days.

Step 6 — Receive and Review Your Sanction Letter

Once the credit assessment clears, the bank issues your education loan sanction letter. This is one of the most important documents in the entire process, it is what you submit to your university for admission confirmation and to the embassy for your student visa.

The sanction letter contains the following terms, review every one of them carefully before accepting:

- Sanctioned loan amount — verify this covers your full cost of attendance, not just tuition

- Interest rate — note whether it is fixed or floating, and which benchmark rate it is linked to (MCLR or EBLR)

- Loan tenure — total repayment period after moratorium

- Moratorium period — course duration plus 6 or 12 months depending on lender policy

- Margin money requirement — the percentage you must contribute from your own funds (typically 5% for domestic, 15% for abroad)

- Conditions precedent — what the bank requires before releasing the first disbursement (visa stamp, fee demand notice, loan agreement signing)

- Processing fee — typically Rs.10,000 for SBI; 1 to 2% of loan amount for NBFCs

What to verify before accepting:

Check that the sanctioned amount matches what you applied for. If it is lower than expected, ask the loan officer why, sometimes a property valuation came in low or the FOIR calculation was tighter than expected. These are negotiable in some cases.

Check the moratorium terms carefully. Some lenders start charging simple interest from disbursement day. Others capitalise unpaid moratorium interest into the principal. The difference in total repayment can be Rs.2 to Rs.5 lakh on a Rs.30 lakh loan.

Read the prepayment clause. Some lenders charge a penalty for early loan closure. If you plan to repay the loan faster after getting a job, a zero-prepayment-penalty clause saves you meaningfully.

Step 7 — Sign the Loan Agreement

The loan agreement is the binding legal contract between you, your co-applicant, and the bank. It follows the sanction letter and precedes disbursement.

Signing happens at the bank branch and typically requires the physical presence of both the student and the co-applicant. For collateral loans, the property owner (if different from the co-applicant) must also be present.

Read the loan agreement carefully before signing. Do not sign anything that was not disclosed in the sanction letter. Pay particular attention to:

- The exact interest rate clause and reset frequency (for floating rate loans)

- The moratorium period terms and what happens to interest during that period

- The disbursement schedule — which expenses are covered in each tranche

- The default and recovery clause

- Any insurance requirement (some banks require a life insurance policy on the co-applicant as a condition)

Once signed, the bank registers the loan and initiates disbursement processing.

Step 8 — Disbursement: How and When Money Is Released

Disbursement is not a single transfer, it is a staged process tied to your institution’s fee schedule.

Tuition fee disbursement: The bank transfers tuition fees directly to the institution’s designated fee account. You will never see this money in your personal account. The bank requires a fee demand letter from the institution (or the admissions offer letter specifying fees due) before each tuition disbursement.

Living expense disbursement: For study abroad loans, living expense components are released to your bank account in tranches, typically once per semester. For domestic loans, banks usually disburse the complete approved amount to the institution.

Timeline: First disbursement happens 3 to 7 working days after the loan agreement is signed, provided all conditions precedent are met, meaning your visa is stamped (for abroad loans), your fee demand notice is submitted, and all property registration is complete (for secured loans).

One critical rule: Do not assume disbursement will happen automatically. You must actively submit the fee demand notice to your bank at least 10 working days before your institution’s fee payment deadline. Banks need time to process the transfer.

Step 9 — Apply for Government Interest Subvention (If Eligible)

This step is separate from the loan application itself and is missed by a significant number of eligible students.

If your annual family income is up to Rs.8 lakh and you are studying at one of the 902 Quality Higher Educational Institutions (QHEIs) listed under PM Vidyalaxmi, you qualify for a 3% interest subvention during the moratorium period. If your income is up to Rs.4.5 lakh and you are in a technical or professional course, you qualify for full interest subsidy under CSIS.

Apply for this through the PM Vidyalaxmi portal after your loan is sanctioned and the first disbursement occurs. The process requires uploading your income certificate and loan sanction details. The subsidy amount is credited to the PM Vidyalaxmi Digital Rupee App (CBDC Wallet) of the beneficiary and on redemption on the app by the beneficiary, the amount is transferred to the beneficiary loan account.

Download and activate the PM Vidyalaxmi Digital Rupee App using your Aadhaar-linked mobile number. This is a mandatory step to receive the subsidy, the funds will not transfer automatically without it.

Public Bank vs Private Bank vs NBFC: Which Should You Apply to First?

This question deserves a direct answer because most competing guides avoid it.

Apply to a public bank first if your co-applicant’s CIBIL score is above 720, you have a property to offer as collateral, and your target institution is widely recognised. Public banks offer the lowest interest rates and longest tenures in the market. The slower processing is a worthwhile trade-off for a rate difference that saves Rs.3 to Rs.5 lakh over a 12-year loan tenure.

Apply to an NBFC first if your visa interview date is within 3 weeks, you need a large unsecured loan (above Rs.40 lakh), your institution is newer or not on a public bank’s list, or your previous public bank application was declined. NBFCs approve faster, cover more institutions, and use more flexible underwriting.

Apply to both simultaneously if your timeline is tight and the institutions you are applying to are on both lender types’ eligible lists. This is a reasonable strategy, two concurrent applications do not damage your CIBIL score materially if done through the Vidya Lakshmi portal.

Common Mistakes During the Application Process

Starting too late. The most consistent pattern I see is students applying 2 to 3 weeks before their first fee deadline. A public bank loan can take 25 working days. Add 7 days for disbursement setup. That is already 32 working days — more than 6 calendar weeks. Start a minimum of 8 weeks before your first fee payment date.

- Submitting documents with name mismatches. If your Aadhaar says “Rahul Kumar Sharma” and your Class 10 marksheet says “Rahul K. Sharma,” the bank will flag it. Every document across the entire set must match perfectly. Check every single document before submission.

- Not following up after submitting. Regularly check the application status on the Vidya Lakshmi portal and respond quickly to any requests from the bank. A file that sits “on hold” for 5 days waiting for your response has effectively wasted 5 days of your processing timeline.

- Choosing a lender based only on the interest rate. A rate that is 0.5% lower but comes with a 25-day processing time versus 7 days can cost you your university seat if you are working against a deadline. Factor total cost of borrowing alongside speed of processing when comparing lenders.

- Not asking about government subsidy schemes. Many bank relationship managers focus on closing the loan application without mentioning CSIS or PM Vidyalaxmi eligibility. Take the initiative — ask explicitly whether you qualify for any interest subvention scheme.

- Applying to multiple lenders simultaneously outside the Vidya Lakshmi portal. Direct applications to three different banks creates three separate hard inquiries on your co-applicant’s CIBIL report, each causing a small score dip. The Vidya Lakshmi portal is designed to avoid this, use it.

Frequently Asked Questions

How long does the education loan application process take in India?

The complete process from application submission to first disbursement takes 3 to 6 weeks depending on the lender. Public banks take 15 to 25 working days for credit assessment. NBFCs take 4 to 7 working days. Disbursement follows 3 to 7 working days after the loan agreement is signed. Start at least 8 weeks before your first fee payment deadline.

What documents do I need to apply for an education loan?

You need student KYC documents (Aadhaar, PAN, passport), academic marksheets, the university admission letter, the fee structure, co-applicant income proof (salary slips, ITR, bank statements), and collateral documents if applicable (property papers, FD certificates). A complete document set submitted upfront cuts processing time significantly.

Can I apply for an education loan online in India?

Yes. The PM Vidya Lakshmi portal at pmvidyalaxmi.co.in allows students to submit one application form to up to three banks simultaneously and track status online. Most NBFCs also offer fully digital application processes with in-principle approval within 24 to 48 hours.

Is a co-applicant mandatory for an education loan?

Yes, a co-applicant is mandatory for most education loans above Rs.4 lakh because students typically have no income. The co-applicant (usually a parent or guardian) is jointly responsible for repayment and their CIBIL score and income are central to the bank’s approval decision.

What is the minimum CIBIL score needed for an education loan?

For unsecured loans from private banks and NBFCs, a co-applicant CIBIL score of 700 or above is generally required. For secured loans at public banks with collateral, 650 is often acceptable. A score above 750 typically qualifies for the best rate bands.

What happens after my education loan is sanctioned?

After receiving your sanction letter, you use it for university admission confirmation and visa applications. You then sign the formal loan agreement at the bank branch. After signing, the bank disburses tuition fees directly to the university and living expense funds to your account as per the agreed schedule.

Can I switch lenders if my education loan is rejected?

Yes. A rejection by one lender does not prevent you from approaching others. Different lenders have different eligibility criteria, a public bank rejection on collateral grounds may not apply to an NBFC. Identify the specific rejection reason before reapplying, and ensure the next application addresses that issue directly.

Is the PM Vidya Lakshmi portal free to use?

The Vidya Lakshmi Education Loan Portal is a government-sponsored programme and students do not have to pay any registration or application fee. When any third party requests money to secure a loan using this portal, they are likely scammers.

Apply Education Loan At GradsLoan Today

Applying for an education loan in India doesn’t have to be overwhelming. Whether you’re heading to an IIT, a top private university, or studying abroad, GradsLoan helps you find the right loan, at the right rate, with the least paperwork. From government bank loans under the Vidya Lakshmi portal to private lenders and NBFCs, we guide you through every step, eligibility, documents, collateral rules, and disbursement. Thousands of Indian students secure funding every year. With the right guidance, you can too. Start your application today and take the first step toward your degree without the financial stress.

Conclusion

Applying for an education loan in India in 2026 is more accessible than ever, the PM Vidya Lakshmi portal, digital NBFCs, and expanded government subsidy schemes have removed many of the barriers that used to make this process unnecessarily painful.

The families that navigate this process smoothly are the ones who start early, gather their documents before approaching any lender, check their co-applicant’s CIBIL score proactively, and choose their lender based on their specific profile rather than name recognition.

Follow the eight steps in this guide in sequence, give yourself at least 8 weeks before your fee deadline, and submit the most complete possible document set from day one. The loan will follow.

Disclaimer: Processing times, eligibility criteria, interest rates, and portal features are sourced from official bank and government resources as of April 2026 and are subject to change. Always verify current details directly with your lender or at pmvidyalaxmi.co.in before applying. This article does not constitute financial advice.